Super Surplus Insurance Policy

The Star Super Surplus Insurance Policy is a top-up health plan designed to extend coverage beyond your existing health insurance. It offers high coverage limits at affordable premiums, providing comprehensive protection for you and your family. With the Star Super Surplus, you can enhance your health coverage without worrying about high costs. This policy acts as a financial safety net, covering expenses that exceed the deductible limit of your base policy. Ideal for those seeking extensive health coverage, the top-up health insurance plan helps you stay prepared for unexpected medical expenses. This Policy ranks among the most comprehensive health insurance top-up plans available today. Choose the Star Super Surplus to secure your health and financial well-being with confidence. This top-up health insurance plan acts as a financial buffer when your base policy coverage is exhausted.

Top-up insurance like Star Super Surplus ensures you don’t compromise on care due to coverage limits. The Star Health Super Surplus Insurance plan is a kind of effective top-up health insurance policy crafted to offer additional medical coverage apart from your existing health insurance plan. Top-up health insurance serves as an add-on to your primary health coverage, activating when your base policy limit is exceeded. These insurance plans provide tailored medical coverage once the insured amount of your base policy is fully utilised. But the question is, how does top-up health insurance work? A top-up health insurance policy includes a predetermined deductible limit, which the insured must choose at the time of purchase. Claims under this policy become applicable when hospitalisation costs exceed the selected deductible. To maximise coverage, a standard health insurance plan can be used to cover the deductible portion of the top-up policy.

Super Surplus Insurance Policy IRDAI UIN: SHAHLIP22035V062122

Star Super Surplus (Floater) Insurance Policy UIN: SHAHLIP22034V062122

HIGHLIGHTS

Plan Essentials

Top-up Policy

Flexible Policy

Long-Term Discount

Medical Examination

Instalment Options

Individual Entry Age

Floater Entry Age

DETAILED LIST

Understand what’s included

GENERAL FEATURE

Policy TermThis policy can be availed for a term of one or two years. |

Lifelong RenewalThis policy provides a lifelong renewal option. |

INDIVIDUAL PLAN (GOLD)

In-Patient HospitalisationHospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered. |

Pre-HospitalisationIn addition to in-patient hospitalisation, the medical expenses incurred up to 60 days before the date of admission to the hospital are also covered. |

Post-HospitalisationPost-hospitalisation medical expenses up to 90 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause. |

Room RentRoom (Single Private A/C room), boarding and nursing expenses incurred during in-patient hospitalisation are covered. |

Road AmbulanceAmbulance charges including private ambulance incurred for transporting the insured person to the hospital are covered up to Rs. 3000/- per policy period. |

Air AmbulanceAir Ambulance expenses are covered up to 10% of the Sum Insured applicable for Sum Insured of Rs. 7 lakhs and above. |

Modern TreatmentModern treatment expenses incurred either as an in-patient hospitalisation or day care treatment are payable to the extent of the sub-limits mentioned in the policy clause. |

Delivery ExpensesDelivery expenses including the Caesarean section are covered up to Rs. 50,000/- per delivery to the maximum of two deliveries. This can be availed after a 12 month waiting period. |

Organ Donor ExpensesOrgan transplantation expenses are payable subject to the availability of the Sum Insured if the insured person is the recipient. |

Recharge BenefitOn exhaustion of the Sum Insured for the remaining policy period, an additional indemnity is provided once during the policy period up to the specified limits. |

Wellness ServicesWellness programs designed to motivate and encourage the healthy lifestyle of the insured person through various wellness activities. |

E-Medical OpinionE-Medical Opinion facility from the Company’s expert panel is available on the request initiated by the insured person. |

Defined LimitDefined limit means the amount up to which the company will not be liable during the policy period. |

AYUSH Treatment Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured. |

INDIVIDUAL PLAN (SILVER)

In-Patient HospitalisationHospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered. |

Pre-HospitalisationIn addition to in-patient hospitalisation, the medical expenses incurred up to 30 days before the date of admission to the hospital are also covered. |

Post-HospitalisationPost-hospitalisation medical expenses up to 60 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause. |

Room RentRoom (including single standard A/C room), boarding and nursing expenses incurred during in-patient hospitalisation are covered up to Rs. 4000/- per day. |

Modern TreatmentModern treatment expenses are payable to the extent of the sub-limits mentioned in the policy clause. |

DeductibleDeductible means the amount up to which the company will not be liable for each and every hospitalisation. |

AYUSH Treatment Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured. |

FLOATER PLAN (GOLD)

In-Patient HospitalisationHospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered. |

Pre-HospitalisationIn addition to in-patient hospitalisation, the medical expenses incurred up to 60 days before the date of admission to the hospital are also covered. |

Post-HospitalisationPost-hospitalisation medical expenses up to 90 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause. |

Room RentRoom (including single private A/C room), boarding and nursing expenses incurred during in-patient hospitalisation are covered. |

Air AmbulanceAir Ambulance expenses are covered up to 10% of the Sum Insured applicable for Sum Insured of Rs. 10 lakhs and above. |

Road AmbulanceAmbulance charges including private ambulance incurred for transporting the insured person to the hospital are covered up to Rs. 3000/- per policy period. |

Modern TreatmentModern treatment expenses are payable to the extent of the sub-limits mentioned in the policy clause. |

Delivery ExpensesDelivery expenses including the Caesarean section are covered up to Rs. 50,000/- per delivery to the maximum of two deliveries. This can be availed after a 12 month waiting period. |

Organ Donor ExpensesOrgan transplantation expenses are payable subject to the availability of the Sum Insured if the insured person is the recipient. |

Recharge BenefitOn exhaustion of the Sum Insured for the remaining policy period, an additional indemnity is provided once during the policy period up to the specified limits that can be used even for same hospitalisation. |

E-Medical OpinionE-Medical Opinion facility from the Company’s expert panel is available on the request initiated by the insured person. |

Wellness ServicesWellness programs designed to motivate and encourage the healthy lifestyle of the insured person through various wellness activities. |

Defined LimitDefined limit means the amount up to which the company will not be liable during the policy period. |

AYUSH Treatment Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured. |

FLOATER PLAN (SILVER)

In-Patient HospitalisationHospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered. |

Pre-HospitalisationIn addition to in-patient hospitalisation, the medical expenses incurred up to 30 days before the date of admission to the hospital are also covered. |

Post-HospitalisationPost-hospitalisation medical expenses up to 60 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause. |

Room RentRoom (Single Standard A/C Room), boarding and nursing expenses incurred during in-patient hospitalisation are covered up to Rs. 4000/- per day. |

Modern TreatmentModern treatment expenses are payable to the extent of the sub-limits mentioned in the policy clause. |

DeductibleDeductible means the amount up to which the company will not be liable for each and every hospitalisation. |

AYUSH Treatment Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured. |

STAR HEALTH

Why Choose Star Health Insurance?

As a Health Insurance specialist, we extend our services from offering tailor-made products to fast in-house claim settlements. With our growing network of hospitals, we ensure easy access to fulfill your medical needs.

Wellness Program

Diagnostic Centres

E-Pharmacy

GET STARTED

Be Assured of the Best

Get your future secured with us.

Want more information?

Ready to get your policy?

Super Surplus Insurance Policy / Star Super Surplus (Floater) Insurance Policy

“Insurance for Health is Wealth” has become a prominent term in our fast-paced world today. No matter how conscious we are of our mind and body, a health emergency may come knocking at any point in life. You must ensure that you are well-prepared for such circumstances.

A health insurance policy helps you get timely treatment while facing an illness/injury. Even with a standard health insurance policy, rising medical costs can quickly exceed a sum insured of 5–10 lakhs. In such cases, a top-up health insurance plan works as a supplement to your regular health insurance cover. This plan adds additional coverage to your existing health insurance policy. In simple words, a top-up health insurance plan activates once your base policy reaches its coverage limit, offering extended protection.

Star Health Super Surplus Policy is a premium health insurance plan that provides much more coverage than standard health insurance plans. The policy is available on a floater and individual basis, and individuals between the ages of 18 and 65 are eligible to purchase the policy.

When purchased on a floater basis, the policy can cover self, spouse, and dependent children. The policy offers a higher sum insured at an affordable premium, making it a preferred choice for many.

For those seeking to enhance their medical insurance affordably, the Star Health Super Surplus Top-Up Plan is an excellent choice.

The Star Health Super Surplus Policy is available in two plans: Silver Plan and Gold Plan. The policy covers organ donor expenses, daycare treatments, ambulance charges, inpatient hospitalisation expenses, pre-hospitalisation, and post-hospitalisation expenses.

What is Super Top-up health insurance?

A super top-up health insurance plan kicks in once the total medical expenses within a policy year exceed the deductible limit.

For instance, if you have a base health plan with a sum insured of Rs. 5 lakhs and an additional super top-up plan of Rs. 3 lakhs. In case of hospitalisation, your base health plan will bear the costs of medical bills up to Rs. 5 lakhs, and the top-up plan will kick in after the maximum sum assured by your base plan has been crossed.

Top-up Health Insurance Plan

A health insurance top-up is an additional coverage plan that supplements your existing health insurance policy. It comes into effect once your base policy’s sum insured is exhausted, offering financial protection against high medical expenses without the need to upgrade your primary plan.

A top-up health insurance plan offers extra medical coverage for individuals already covered by a personal or employer-provided health policy.

This type of insurance enhances your existing individual or group mediclaim policy by offering additional medical coverage. It enhances the degree of financial security you have against different health-related concerns and expands the sum insured amount.

If your health insurance policy does not provide enough coverage to meet high hospitalisation bills, you may have to purchase two insurance policies or increase the sum assured amount.

Whether you're looking to protect your savings or prepare for rising healthcare costs, a health insurance top-up is a smart and affordable way to boost your coverage. Select a top-up health insurance plan that aligns with your needs and strengthens your financial protection against medical expenses.

Example

Suppose you have a health plan with a maximum sum assured of Rs. 10 lakhs, and you take a top-up plan for Rs. 4 lakhs. If you're hospitalised, your base plan will cover expenses up to Rs. 10 lakhs, and the top-up plan will cover costs beyond that limit.

A top-up health insurance plan is an add-on cover that increases the health insurance coverage for the policyholder.

When medical bills exceed your insurance coverage, out-of-pocket expenses can threaten financial stability. In such cases, top-up plans offer valuable support.

Star Health’s Super Surplus Insurance Policy offers coverage up to one crore at an affordable premium, making it a strong supplement to your existing health plan. It provides broader protection compared to standard health insurance plans. The policy is available for the age group from three months to 65 years on both an individual and a floater basis.

The policy is available in options as Gold and Silver plans. The waiting period under this policy is 12 months and 36 months, respectively. The policy terms are one year/2 years. On the policy purchase, a lifelong renewability option is available.

Can we top up Health Insurance?

Yes, a person can top up his/her health insurance policy to offer extra coverage. A top-up health insurance policy is an add-on to your existing health insurance plan. It provides extra coverage once your medical expenses exceed a certain deductible. We have seen what a top-up in health insurance is; let’s see how to top up health insurance.

How to top up Health Insurance?

You can avail a top-up health insurance in two ways, either as a top-up health plan or as a super top-up health plan. Both of these ways function as a booster to your primary health insurance policy. These plans could be used to pay the extra medical expenses if your regular health policy gets exhausted.

Can we take a Top-Up on Health Insurance?

Know how to take top-up health insurance. As mentioned above, the top-up health insurance is an extra health coverage that you could add to your existing health insurance policy that you have.

In our country, in some cases, your basic health plan might not be sufficient, as there is an increase in lifestyle ailments and medical inflation due to modernisation. In India, top-up health insurance can help bridge the gap caused by rising medical costs and lifestyle-related illnesses.

Hence, choosing a top insurance alone is not enough; you could also select the best top-up health insurance. Here, we have already discussed top-up health insurance benefits.

When you check what the top health insurance company is, also check the details of the top-up health insurance provided by those companies. Explore the best insurance plan and the best top-up health insurance that suits your medical and financial needs.

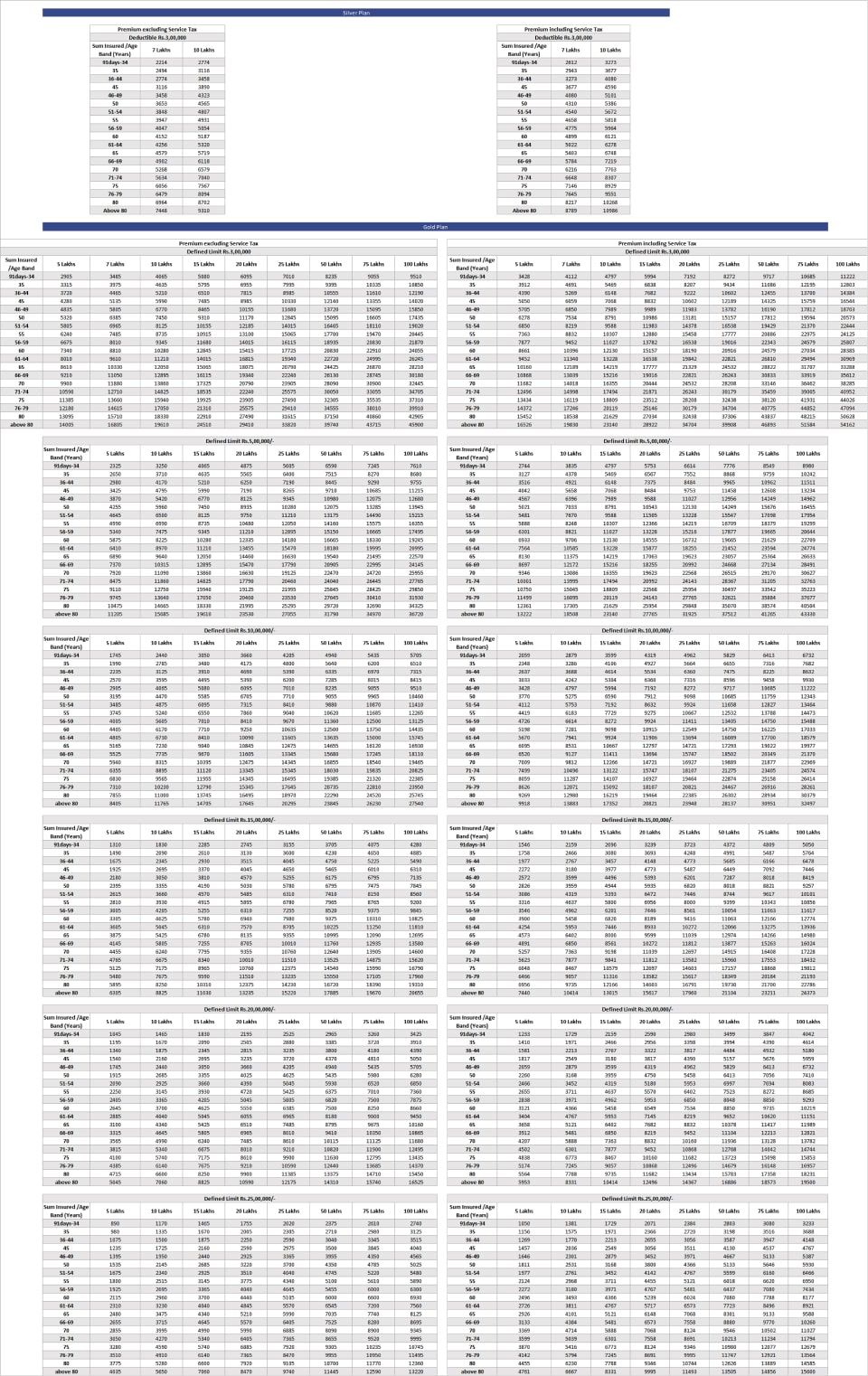

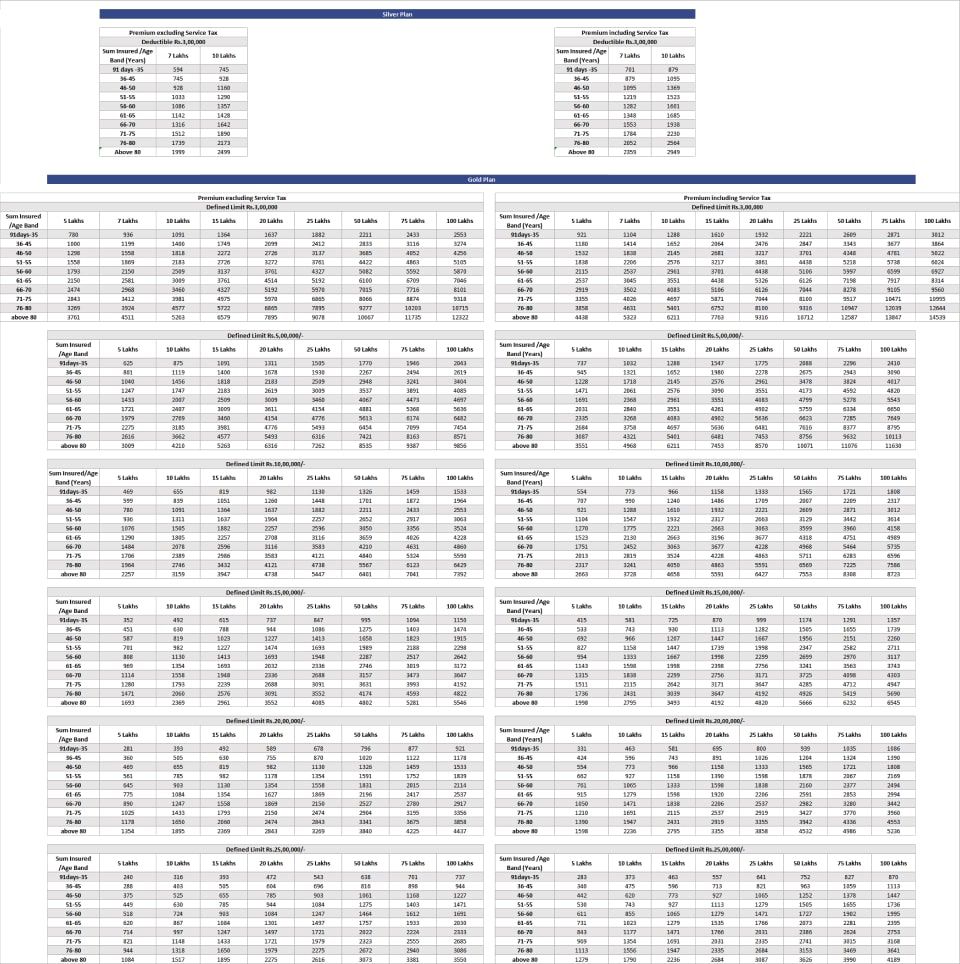

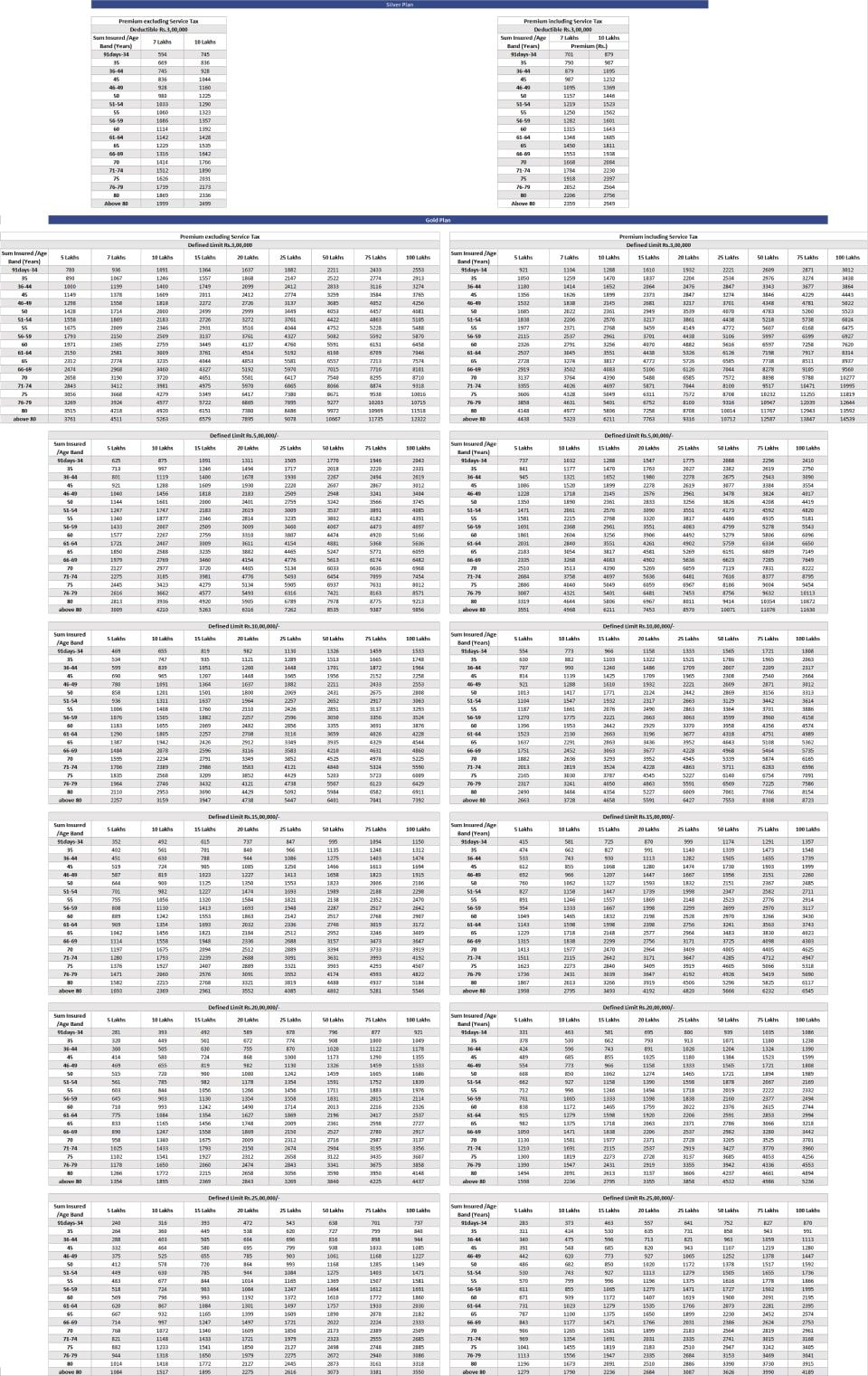

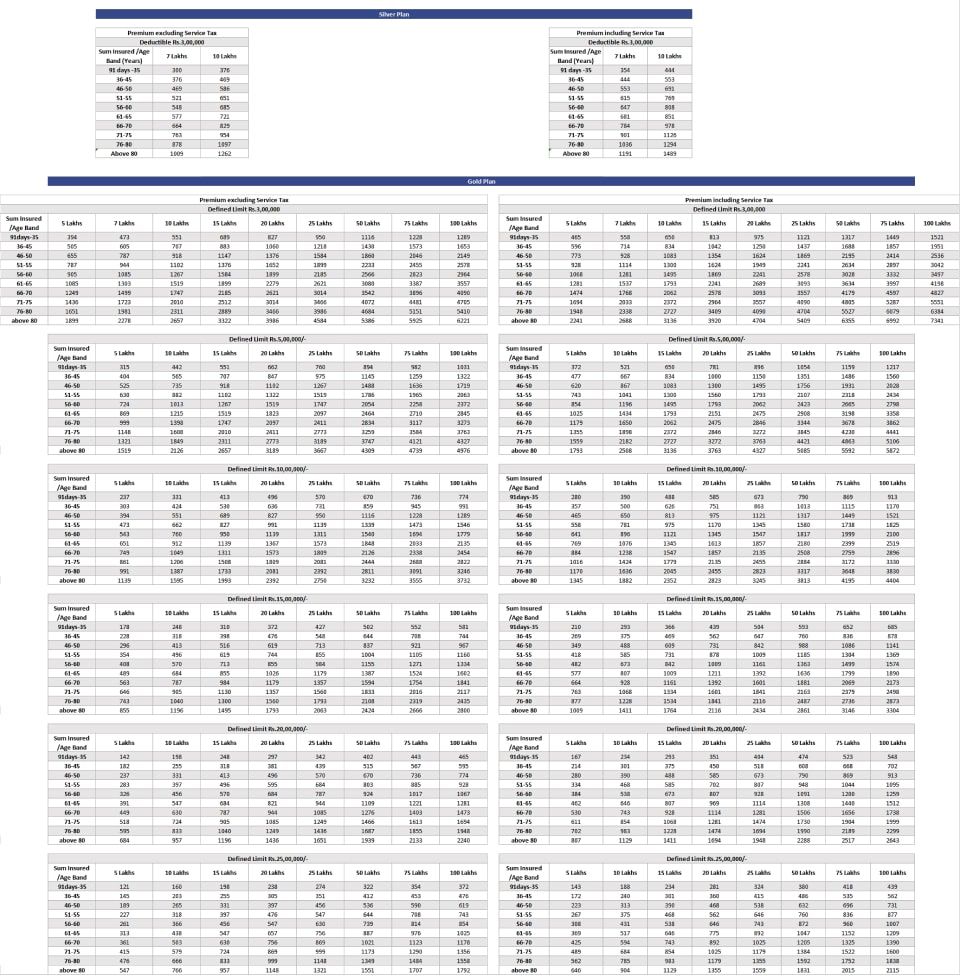

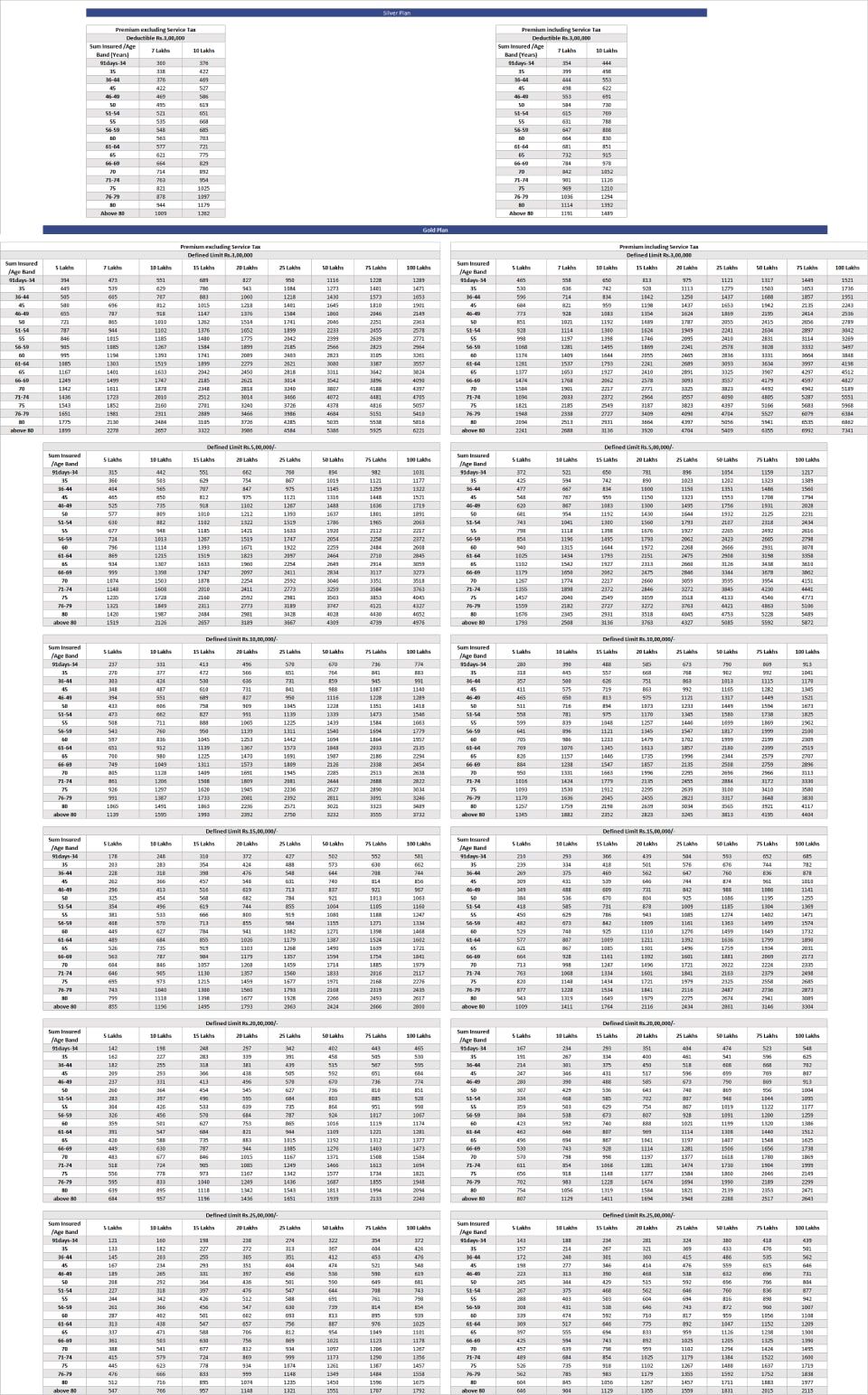

Features of Super Surplus Health Insurance Policy

| S.No | Subject | Criteria | ||

|---|---|---|---|---|

| 1. | Eligibility | 18-65 years | ||

| 2. | Dependent children | 91 days to 25 years | ||

| 3. | Policy term | 1 / 2 years | ||

| 4. | Plan options | Silver / Gold plan | ||

| 5. | The company will pay in excess of the deductible limit on every claim under the Silver plan. | Silver | Sum insured | Deductible limit |

| Individual | 7 lakhs / 10 lakhs | 3 lakhs | ||

| Floater | 10 in lakhs | 3 & 5 lakhs | ||

| The company will pay the aggregate of all claims amounts in excess of the defined limit in the policy year under the Gold plan | Gold | Sum insured | Defined limit | |

| Individual | 5 / 10 / 15 / 20 / 25 /50 / 75/ 100 lakhs | 3 / 5 /10 / 15 / 20 /25 lakhs | ||

| Floater | ||||

| 6. | Product type | Individual / Floater | ||

| 7. | Installment facility | Quarterly / Half-yearly | ||

| 8. | Discounts | 5 per cent discount only if the entire two-year premium is paid in advance | ||

| 9. | Renewals | Life-long renewal option | ||

| 10. | Pre-insurance medical screening | Not required | ||

Coverage under Super Surplus Insurance Policy / Star Super Surplus (Floater) Insurance Policy

The policy offers extensive coverage for both individual and floater under two plan options, namely Gold and Silver. You can use the super top-up health insurance premium chart to compare Gold and Silver plan options by coverage and cost. These top-up health insurance plans offer flexibility for both individual and floater coverage, ensuring tailored protection.

This benefit is elaborated as follows:

Individual Plan (Silver)

- In-hospitalisation Expenses- Expenses such as room, boarding and nursing expenses are subject to a maximum of Rs. 4000 per day. Other expenses like surgeon’s fee, anaesthetist, medical practitioner, consultants, specialist fee, blood, oxygen, ICU charges, operation theatre charges, medicines and drugs, diagnostic materials and lab tests are also covered.

- Pre-hospitalisation Expenses- Expenses incurred up to 30 days before getting hospitalised are covered.

- Post-hospitalisation Expenses- Expenses incurred up to 60 days after discharge are covered.

- Coverage for Modern Treatments- Modern/Advanced treatments are covered under the policy for the specific illness up to the sub-limit mentioned in the policy clause.

Individual Plan (Gold)

- In-hospitalisation Expenses-Expenses like room (single Private AC room), boarding and nursing as provided by the hospital are covered. Other expenses like surgeon’s fee, anaesthetist, medical practitioner, consultants, specialist fee, blood, oxygen, ICU charges, operation theatre charges, medicines and drugs, diagnostic materials and lab tests are also covered.

- Pre-hospitalisation Expenses-Expenses incurred up to 60 days before getting hospitalised are covered.

- Post-hospitalisation Expenses- Expenses incurred up to 90 days after discharge are covered.

- Coverage for Modern Treatments- Modern/Advanced treatments are covered under the policy for the specific illness up to the sub-limit mentioned in the policy clause.

- Emergency ambulance charges- Emergency ambulance charges up to Rs. 3,000 per policy period for the transportation of the insured to the hospital are applicable.

- Air ambulance charges- Air ambulance expenses are covered up to 10 per cent of the sum insured per policy period (only applicable for sum insured Rs. 7,00,000 and above).

Floater Plan (Silver)

- In-hospitalisation Expenses-Room, boarding and nursing expenses are subject to a maximum of Rs. 4000 per day. Other expenses like surgeon’s fee, anaesthetist, medical practitioner, consultants, specialist fee, blood, oxygen, ICU charges, operation theatre charges, medicines and drugs, diagnostic materials and lab tests are also covered.

- Pre-hospitalisation Expenses- Expenses incurred up to 30 days before getting hospitalised are covered.

- Post-hospitalisation Expenses- Expenses incurred up to 60 days after discharge are covered.

- Coverage for Modern Treatments- Modern/Advanced treatments are covered under the policy for the specific illness up to the sub-limit mentioned in the policy clause.

Floater Plan (Gold)

- In-hospitalisation Expenses- Expenses like room (single Private AC room), boarding and nursing as provided by the hospital are covered. Other expenses like surgeon’s fee, anaesthetist, medical practitioner, consultants, specialist fee, blood, oxygen, ICU charges, operation theatre charges, medicines and drugs, diagnostic materials and lab tests are also covered.

- Pre-hospitalisation Expenses- Expenses incurred up to 60 days before getting hospitalised are covered.

- Post-hospitalisation Expenses- Expenses incurred up to 90 days after discharge are covered.

- Coverage for Modern Treatments- Modern/Advanced treatments are covered under the policy for the specific illness up to the sub-limit mentioned in the policy clause.

- Emergency ambulance charges- Emergency ambulance charges up to Rs. 3,000 per policy period forthe transportation of the insured to the hospital is applicable.

- Air ambulance charges- Air ambulance expenses are covered up to 10 per cent of the sum insured per policy period (only applicable for sum insured Rs. 10,00,000 and above).

How does a Top-up Health Insurance Plan work?

A top-up mediclaim policy is ideal for individuals who want to extend their coverage without replacing their existing plan. To understand the working of top-up policies, you should know two terms: one is Deductible & Defined Limit (Aggregate Deductible)

- Deductible–A deductible is an amount the policyholder agreed to pay for every admissible hospitalisation claim. The top-up for health insurance becomes active only after the deductible threshold is crossed, making it a cost-effective solution.

- Defined Limit(Aggregate Deductible)– A defined limit is an aggregate amount of admissible claims the policyholder has agreed to pay during the policy period.

Health insurance top-up options like this allow policyholders to manage high medical bills without upgrading their base plan.

Case Study: Top-up health insurance is especially useful when your primary policy has a lower sum insured. For example, if the insured has a top-up policy with a sum insured of 10 lakhs and a deductible of 1 lakh, the plan provides additional coverage beyond the deductible.

Case study on opting for Top-up with Deductible

| Period of Claim Claims during the same year | Claims during the same year | Sum Insured (Deductible) | Insured to pay for each Claim | Admissible claim Amount Payable | Amount payable | Balance the sum insured available for future claims |

| 21- 22 | 1st | 10 lakhs (1L) | 1 Lakh | 5 Lakhs | 4 Lakhs | 6 lakhs |

| 21- 22 | 2nd | 6 Lakhs (1L) | 1 Lakh | 3 lakhs | 2 lakhs | 4 lakhs |

| 21- 22 | 3rd | 4 Lakhs (1 L) | 1 Lakh | 4 lakhs | 3 lakhs | 1 lakh |

| 21- 22 | 4th | 1Lakhs (1L) | 1 Lakh | 2 lakhs | 1 lakh | nil |

Case study on opting for Top-up with Defined (Aggregate Deductible)

| Period of Claim | Claims during the same year | Sum Insured (Defined ) | Insured to pay for each policy period | Admissible claim Amount Payable | Amount payable | Balance the sum insured available for future claims |

| 21- 22 | 1st | 10 lakhs (1 lakh) | 1 Lakh | 5 Lakhs | 4 Lakhs | 6 lakhs |

| 21- 22 | 2nd | 6 lakhs | Nil | 3 Lakhs | 3 lakhs | 3 lakhs |

| 21- 22 | 3rd | 3 Lakhs | Nil | 3 Lakhs | 3 lakhs | nil |

In this case, the health insurance top-up plan activates once the deductible of ₹1 lakh is met.

Investing in a top-up health insurance plan not only provides financial freedom but also a sense of security, ensuring peace of mind.

- Cost-effective protection against ever-rising medical treatment costs.

- People who have to pay more than the coverage given by their employer,

- People who have lower coverage under their individual/family coverage.

- Those who can convert their top-up plan to a regular cover, post-retirement, with renewal benefits.

- You can claim tax deduction under Section 80D of the Income Tax Benefit.

Health insurance specialists say that a top-up plan is a must-have as unexpected medical emergencies can cause a major financial hardship during hospitalisation. However, buying a top-up plan is much better than extending your existing basic health insurance cover at a nominal cost. Top-up health insurance plans are designed to provide additional cover if your existing policy gets exhausted.

What are the inclusions and exclusions of the policy?

The Super Surplus Insurance Policy comes with certain inclusions (covered) and exclusions (not covered). They are as follows:

Inclusions

- The Super Surplus Gold plan offers coverage for maternity up to specified limits.

- Provides air ambulance cover for up to 10% of the sum insured for more than Rs. 7 lakhs (individual) and 10 lakh (floater).

- Coverage for organ donor expenses.

- Coverage for inpatient hospitalisation expenses.

- Pre- and post-hospitalisation expenses are also covered.

- Cover for all day-care procedures or treatments (under the gold plan).

- Coverage for pre-existing diseases under the Super Surplus Silver Plan is 36 months, and specific treatments have a 24-month waiting period.

- Coverage for pre-existing diseases under the Super Surplus gold plan is 12 months, and specific treatments have a 12-month waiting period.

Exclusions

The following is a partial listing of policy exclusions. A detailed list of all exclusions is included in the policy document.

- Any ailment/injury caused by war, civil war, biological war, etc.

- Self-intentional injuries like suicide attempts.

- Costs of walkers/wheelchairs.

- Expenses related to treatment for weight loss surgeries.

- Cosmetic or plastic surgery expenses are not covered unless they are the result of an accident.

- Expenses related to injuries caused by hazardous sports or adventurous activities.

- Expenses related to the change of gender treatments and sexually transmitted diseases.

What does a Top-up health insurance Plan offer?

A top-up health insurance plan prepares you for increasing and dynamic costs of hospitalisation. It is similar to that of any regular health insurance plan. This plan is payable towards treatment expenses for illness or accidents in a hospital or day-care centre. The maximum amount policyholders must pay is deductible before their insurer covers the losses. A higher deductible lowers the premium. The waiting period for pre-existing and specified illnesses is 12 months from the policy's inception under the defined limit.

Advantages of top-up health insurance plans

- Enhanced coverage: A top-up plan allows people to enhance their medical coverage so that they can pay for unforeseen medical expenses even after the sum insured of their base policy is exhausted.

- Lower premium: Top-up health insurance options are designed to provide comprehensive coverage at a lower cost, so you won’t need to buy a new health insurance policy.

- Tax benefits: You may be eligible for tax benefits on the top-up policy premium you pay under Section 80D of the Income Tax Act of 1961. The cost of insurance for oneself, one’s spouse, and dependent children might lower your tax obligation by up to INR 25,000.

Senior citizens may enjoy a higher limit of deduction, and if you are over 60 years of age, you may claim a deduction of up to INR 50,000. - Coverage for Pre-existing diseases: Generally, health plans do not offer coverage against pre-existing diseases. However, you may supplement your base plan with a top-up that offers the same coverage. This proves beneficial in case you have a family history of certain illnesses, such as hypertension or diabetes.

- Tackle rising medical inflation: Medical inflation in India is increasing at an alarming rate of around 20% as compared to 8-9% in the past few years. Thus, investing in a top-up health insurance policy can help you combat such inflation effectively.

How do top-up plans differ from regular insurance plans?

Top-up health insurance plans cover almost all hospitalisation expenses and provide the same benefits as a basic health plan. The key difference is the deductible, which makes these plans more affordable. Most top-up plans do not require pre-medical screening up to the age of 50 years, which is mandatory after 45 years under most basic health insurance plans.

If your basic health plan reaches the sum insured limit, you can file a claim under both your base plan and top-up plan together. Moreover, you can easily file a claim under both plans simultaneously with insurance providers, who will be liable to pay off part of their claims.

Things covered in the Top-up Health Insurance Plan

Inpatient hospitalisation expenses

In-patient hospitalisation expenses, including nursing and boarding charges, room rent, doctors’ fees, OT charges, cost of oxygen, prosthetic devices or implantation of any other equipment during surgery, blood, diagnostic procedures and other similar expenses.

- Pre-hospitalisation expenses

- Post-hospitalisation expenses

- Day care procedures that do not require hospitalisation for even 24 hours

- Organ donor expenses

- Emergency ambulance charges

- Domiciliary treatment expenses

Primary things to look for when buying top-up insurance

To select an affordable top-up health insurance plan, opt for higher deductibles. Avoid buying an expensive plan to cover exclusions like daily cash allowance and dental cover, as they may be covered by your regular health insurance policy.

What are the Factors that Influence Choosing the Top Medical Insurance Companies in India?

A mediclaim top-up plan can help bridge the gap between your employer-provided coverage and actual medical expenses. There are several top medical insurance companies in India to choose from. When you choose a medical insurance company in India, you can consider factors like:

- Claim settlement ratio: It denotes the ratio of how well the company settles claims. Select an insurance company with the highest claim settlement ratio.

- Coverage: Check if the company offers insurance plans with coverage for critical illnesses, hospitalisation, and other treatments.

- Sum insured: The sum insured is the maximum amount of coverage that the medical insurance policy provides.

- Waiting Period: The period after which you will receive insurance coverage. It is the period one must wait before the policy takes effect.

- Solvency ratio: The solvency ratio depicts the company's financial stability.

- Renewability: Check if the medical insurance company offers policies that can be renewed over time.

- Network hospitals: Check if the insurance company you select has a network of hospitals for inpatient and out-patient care.

- Critical illness insurance: Check if the insurance company offers a policy that includes coverage for the cost of treatment for critical illnesses.

- Family floater: Whether the policy covers multiple family members under one sum insured.

Things to Consider when Choosing a Top Medical Insurance

When choosing medical insurance, you can consider some factors, such as your needs, coverage, and the insurance provider.

- Healthcare needs: Check for some factors like your medical history, age, and lifestyle.

- Medical expenses: Check how many times you need to go to the hospital, consult a specialist, or get diagnostic tests.

- Sum insured: Choose a medical insurance policy with a high enough sum insured to meet your health needs.

- Family history: See if there is a family history of illnesses.

- Sub-limits: See the limits on room rent and other things.

- Co-payment: See how much you'll pay out of pocket for particular medical services.

- Claim settlement ratio: As mentioned above, choose the insurance company with the highest claim settlement ratio. This is because the claim settlement ratio refers to the claims the insurance provider settled compared to how many are received per year.

- Network of Hospitals: Consider how many hospitals the insurance provider has in your area.

- Day-care procedures: See if the policy offers coverage for day-care procedures such as cataract surgery.

- Policy terms: Check for the policy's exclusions, renewal options and other waiting periods.

- Premiums: Compare the premiums of different medical insurance plans.

- Reviews: Also consider the insurance provider's reviews.

- Extra Considerations: The cost of medical treatment in India is rising, so a higher sum insured may be wise.

- Family floater plans: Family floater plans can be affordable as they provide coverage for multiple family members under one sum insured.

- Cashless claims: See how to make cashless claims and what documentation is required.

- Lifetime Renewability: See if the health insurance policy can help you avoid purchasing a new policy every few years.

By considering all these factors, you could shortlist the top medical insurance companies in India. Then, choose the best one out of the top medical insurance companies in India.

What are the add-on benefits of the Star Super Surplus (Floater) Insurance Policy?

- Additional coverage: The Star Super Surplus (Floater) Insurance Policy acts as a super top-up health insurance plan that offers additional coverage when your basic health plan gets exhausted. The plan comes with a higher sum insured at an affordable premium.

- No pre-insurance medical screening: Generally, while purchasing a health insurance policy, insurers require a pre-medical examination before issuing the policy. The Star Super Surplus (Floater) Insurance Policy doesn’t require any pre-insurance medical screening.

- Free E-medical consultation:The exclusive feature “Talk to Star” offered by Star Health is a free consultation line for customers all over India. You can get in touch with our in-house doctors for a free medical consultation over the phone regarding your health conditions.

- Tax Benefits: Under the Star Super Surplus (Floater) Insurance Policy, the premium paid by any mode other than cash is eligible for tax benefits under Section 80D of the Income Tax Act 1961.

- Free-look period: The policy offers a free-look period of 30 days from the date of receipt of the policy. However, this feature is not applicable for portability, migration and renewals.

How to register a claim for the Star Super Surplus (Floater) Insurance Policy?

Star Health offers hassle-free claim settlement for all its customers. There are two ways through which you can file a claim at your convenience.

Top-up health insurance is a cost-effective way to increase medical coverage. It is advisable to choose a policy with an aggregate deductible and the lowest possible waiting period for pre-existing disease coverage. This helps manage rising medical costs and bridge gaps in corporate, individual, or family health insurance plans.

Super Surplus Policy Automatic Expiry

The insurance coverage under this policy for each insured person will expire upon the earliest of the following events:

- On account of the death of the policyholder or the insured person. The meaning is that the coverage for the surviving members of the family will continue under the other terms of the policy. OR

- On account of the exhaustion of the sum insured below the policy.

Top-up medical insurance is a smart way to extend your coverage without purchasing a new base policy.

Super Surplus Policy Cancellation

The policyholder may cancel his Super Surplus Policy at any time during the term by providing a 7-day written notice. In such a case, the company may:

- Refund the proportionate premium for the unexpired policy period if the policy term is for one year or less and no claim has been made during the policy period.

- Refund the premium for the unexpired policy period, for policies with terms above one year where coverage has not yet commenced.

The company may cancel the policy at any time due to misrepresentation, non-disclosure of material facts, or fraud by the insured person, by providing 15 days’ written notice. Also, there will be no refund of premium on cancellation on the basis of misrepresentation, fraud or non-disclosure of material facts.

Point to Note: If it is a long-term policy, the refund will be given after adjusting the long-term discount obtained by the insured person/ policyholder.

Change of the Policy

The insured person has the choice to migrate to the same health insurance product available with the company during the renewal time, with all the accrued continuity.

Advantages such as cumulative bonus and waiting period waiver, as per IRDAI guidelines, are maintained if the policy has been renewed without a break.

Top-up medical insurance, like this plan, is ideal for individuals and families seeking additional protection beyond their base policy. To ensure comprehensive protection, choose the best top-up health insurance that aligns with your healthcare needs and budget.

FAQ's

People Also Search For

Health Insurance Coverage for pre-existing medical conditions is subject to underwriting review and may involve additional requirements, loadings, or exclusions. Please disclose your medical history in the proposal form for a personalised assessment.

The information provided on this page is for general informational purposes only. Availability and terms of health insurance plans may vary based on geographic location and other factors. Consult a licensed insurance agent or professional for specific advice. T&C Apply. For further detailed information or inquiries, feel free to reach out via email at marketing.d2c@starhealth.in