Star Comprehensive Insurance Policy

The Star Comprehensive Insurance Policy is a robust health insurance plan offering extensive health insurance coverage to meet all your healthcare needs. This health insurance policy includes hospitalisation, pre- and post-hospitalisation expenses, outpatient treatments, and more, ensuring you are well-protected against unexpected medical costs. With this policy, you benefit from a wide range of features, including coverage for daycare procedures, emergency ambulance services, and health checkups. This comprehensive medical insurance policy also provides coverage for alternative treatments like Ayurveda, Unani, Siddha, and Homoeopathy (AYUSH). Ideal for individuals and families seeking all-encompassing health protection, this policy ensures peace of mind and financial security during medical emergencies. Choose this plan for a truly extensive health insurance experience.

IRDAI UIN: SHAHLIP26044V092526

HIGHLIGHTS

Plan Essentials

PED Buy-Back

Bariatric Surgery

Delivery Benefit

Outpatient Cover

Cumulative Bonus

Automatic Restoration of Sum Insured

Personal Accident Cover

Hospital Cash

DETAILED LIST

Understand what’s included

IMPORTANT HIGHLIGHTS

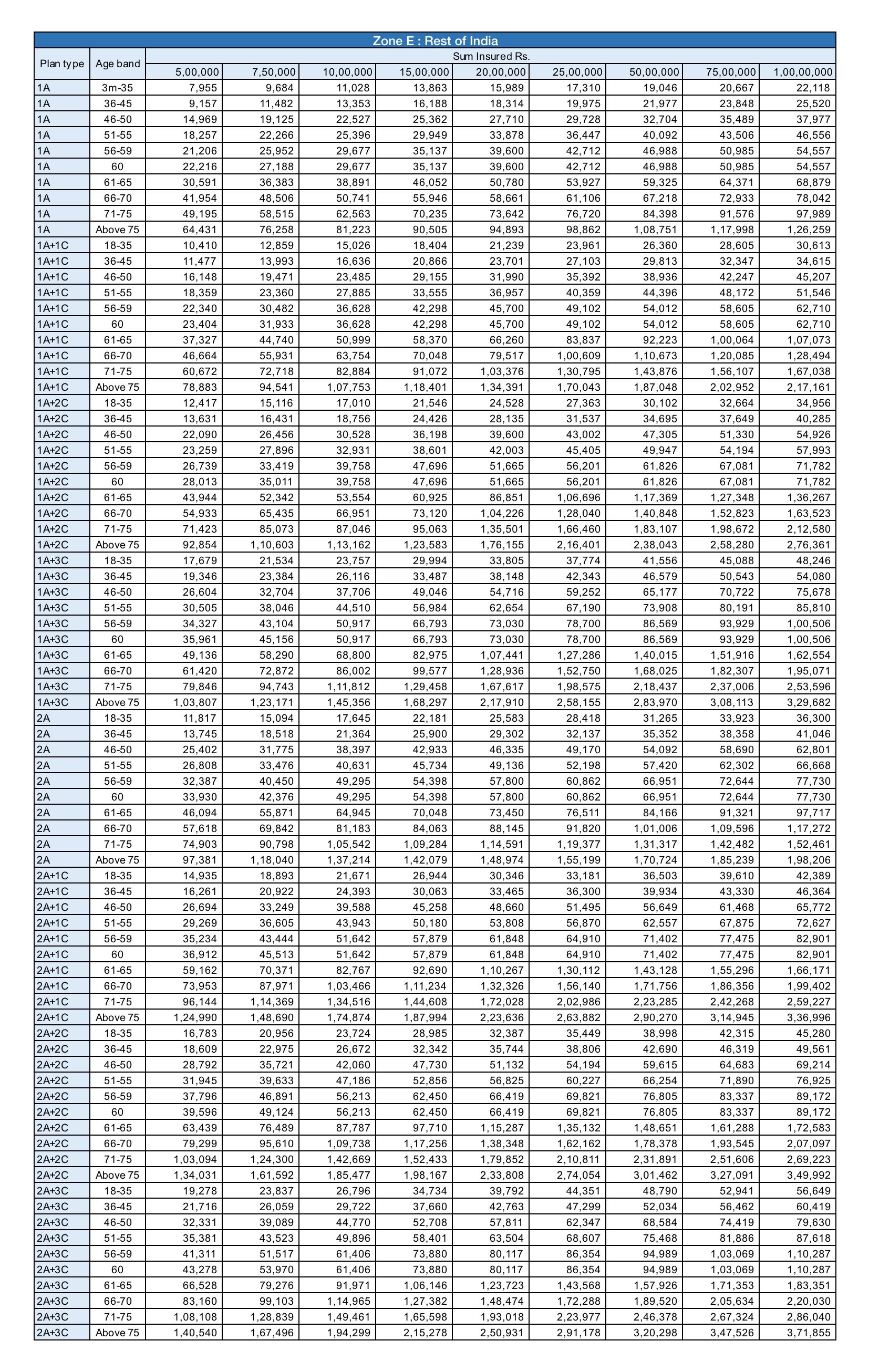

Policy TypeThis policy can be availed either on an Individual or Floater basis. |

Entry AgeAny person aged between 18 and 65 years can avail this policy. Dependent children are covered from the 91st day onwards up to 25 years. |

In-Patient HospitalisationHospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered. |

Pre-HospitalisationPre-hospitalisation medical expenses incurred up to 60 days before the date of admission to the hospital are covered. |

Post-HospitalisationPost-hospitalisation medical expenses up to 90 days from the date of discharge from the hospital are covered. |

Room RentThere is no capping on room rent (Private Single A/C room), Boarding and Nursing expenses under this policy. |

Road AmbulanceThe policy covers ambulance charges for admission to the hospital, shifting from one hospital to another hospital for better facilities and from hospital to the residence. |

Air AmbulanceAir ambulance expenses are also covered up to Rs. 2,50,000/- per hospitalisation, to the maximum of Rs. 5,00,000/- per policy period. |

Mid-Term InclusionThe newly married spouse and newborn baby can be included in the policy by paying an additional premium. The waiting periods will be applicable from the date of inclusion of new joiners. |

Day Care ProceduresMedical treatments and surgical procedures that require less than 24 hours of hospitalisation due to technological advancements are covered. |

Modern TreatmentModern treatment expenses are payable to the extent of the limits mentioned in the policy clause. |

Hospital CashA cash benefit for each completed day in the hospital is provided up to the limits mentioned in the policy clause for a maximum of 7 days per hospitalisation and 120 days per policy period. |

Domiciliary HospitalisationExpenses incurred for domiciliary hospitalisation, including AYUSH, which is taken for a period of more than three days on the advice of a Medical Practitioner are covered. |

Delivery ExpensesDelivery expenses including the Caesarean section (both pre-natal and post-natal) are covered up to the specified limits subject to the maximum of two deliveries. |

New Born CoverThe hospitalisation expenses for the new born baby are covered up to the specified limits based on the opted Sum Insured. |

Vaccination ExpensesVaccination expenses for the new born baby are covered up to the specified limits based on the opted Sum Insured. |

Automatic Restoration of Sum InsuredUpon exhaustion of the basic Sum Insured during the policy period, 100% of the Sum Insured will be restored once in the policy period. |

Co-paymentThis policy is subjected to co-payment of 10% of each and every claim amount for fresh as well as renewal policies for insured persons whose age at the time of entry is 61 years and above. |

Bariatric SurgeryHospitalisation expenses incurred for Bariatric surgical procedures are covered up to the limits of Rs. 2,50,000/- and Rs. 5,00,000/- which are inclusive of pre and post-hospitalisation expenses.

|

AYUSH TreatmentExpenses incurred for the treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in AYUSH Hospitals are covered up to the Sum Insured.

|

Outpatient ConsultationOutpatient expenses other than Dental and Ophthalmic treatments incurred in any Networked Facility are covered up to the limits mentioned in this policy. |

Outpatient Consultation - Dental & OphthalmicOutpatient expenses incurred for Dental and Ophthalmic treatments are covered up to the limits mentioned in the policy clause. The insured person is eligible to avail this benefit after every block of three years. |

Organ Donor ExpensesIn-Patient hospitalisation expenses incurred for organ transplantation from the donor to the recipient insured person are payable provided the claim for transplantation is payable. |

Preventive Health Check-upWe will arrange for a Preventive Health Check-up at Our Network Providers for the applicable package as per opted Sum Insured. For the updated and applicable list of tests available under such package, Insured Persons are required to check our website www.starhealth.in. |

E-Domestic Second Medical OpinionAccess to a second medical opinion from a network doctor based on submitted medical records. |

Star Wellness ProgramWellness program designed to motivate and encourage the healthy lifestyle of the insured person through various wellness activities. In addition, the earned wellness bonus points can be utilised for availing renewal discounts. |

Instalment OptionsThe policy premium can be paid on a monthly, quarterly or half-yearly basis. |

Home Care TreatmentPayable up to 10% of Sum Insured subject to maximum of Rs.5 lakhs in a Policy Year, for treatment availed by the Insured Person at home, only for the specified conditions. |

Unlimited Tele-ConsultationInsured can avail unlimited number of Tele-consultations on Star Health mobile application or digital platforms. |

AI-Driven Face ScanThe Insured Person can avail, AI-driven face scan facility by using Star Health mobile app to know the vital parameters such as heart rate, oxygen saturation, respiration rate up to

two times per month per Insured Person in a Policy Year. |

STAR HEALTH

Why Choose Star Health Insurance?

As a Health Insurance specialist, we extend our services from offering tailor-made products to fast in-house claim settlements. With our growing network of hospitals, we ensure easy access to fulfill your medical needs.

Wellness Program

Diagnostic Centres

E-Pharmacy

GET STARTED

Be Assured of the Best

Get your future secured with us.

Want more information?

Ready to get your policy?

Star Comprehensive Insurance Policy

Star Health Insurance presents the Star Comprehensive Insurance Policy with a pragmatic approach for your lifelong health protection. This plan was specially created for individuals aged 18 to 65 years.

This policy offers several benefits for individuals. It covers all day care procedures, outpatient visits, consultations, adding a newly married spouse or newborn, organ donor expenses, accidental coverage, and other major medical treatments. All of this is included under one sum insured, with lifelong renewal available.

The article is a complete guide to what comprehensive health insurance is, its key features, benefits, importance and more.

What is a Comprehensive Health Insurance Plan?

A comprehensive health insurance plan covers a wide range of medical needs and provides financial protection during emergencies. It can be renewed for life. This plan lets you and your loved ones get coverage together, and you can share the sum insured.

There are many comprehensive medical insurance policy benefits. Let’s discuss the health comprehensive insurance policy inclusions and exclusions here. Many comprehensive health plans include health checkups and daycare procedures, and is suitable for many people based on their needs. We shall have a brief look at the comprehensive health insurance policy.

Key Features of the Star Comprehensive Insurance Policy

- Automatic restoration of the sum insured for both related and unrelated illnesses

- Cumulative bonus accumulation up to 100% of the sum insured

- Coverage for delivery and newborn expenses

Coverage for outpatient consultation, including dental and ophthalmic treatments

Benefits of the Star Comprehensive Insurance Policy

A comprehensive health policy comes with broader coverage. It offers coverage for in-patient hospitalisation costs along with pre- and post-hospitalisation expenses. The benefits of the Star Comprehensive Insurance Policy are listed below:

- Hospitalisation expenses such as boarding charges, room charges, nursing costs, anaesthetist’s fees, specialist fees, drug costs, surgeon’s fees, and medicines can be claimed.

- Pre-hospitalisation charges for up to 60 days before the date of hospitalisation.

- Post-hospitalisation charges for a maximum of 90 days from the date of discharge from the hospital.

- Includes the AYUSH hospitalisation charges like Homoeopathy, Siddha, Ayurveda, and Unani, which are payable below this comprehensive health insurance policy up to the limit as specified under the policy document.

- The road ambulance transportation expenses during emergency conditions are covered.

- Medical consultation expenses incurred by outpatients in a network facility for other than dental and ophthalmic treatments up to the limits mentioned can be claimed.

- Being a member of the comprehensive health plan, you can benefit from domiciliary hospitalisation

- The coverage is available for accidental death and permanent total disability following an accident. Dependent children and persons above 70 years can be covered under accidental death and permanent total disablement up to the sum insured mentioned in the policy document.

- Once every 3 years, the dental/ophthalmic OPD treatment is covered under the policy.

- Hospital cash benefits for a maximum of 7 days per hospitalisation and 120 days for the policy period. However, claims under this section will not lower the sum insured.

- The policy provides cover for delivery and newborn babies, subject to the self and spouse being covered after the completion of the 24-month waiting period.

- The newborn baby is covered from day one, subject to the admissible/ claimed under the policy for delivery.

- The policy provides optional coverage for buyback PEDs, subject to payment of additional premiums and medical screening.

- The policy provides a health check-up benefit for every claim-free year up to the limit specified in the policy.

- This policy can be applied to individual or floater modes.

- The policy provides cover for air ambulance, subject to the terms and conditions, with limits as specified in the policy.

What is included in the Star Comprehensive Health Insurance Plan?

There are many things included under the Star Comprehensive Health Insurance plan. Post-hospitalisation expenses for up to 90 days after being discharged from the hospital.

- Pre-hospitalisation charges and expenses for up to 60 days before getting admitted, and post-hospitalisation expenses incurred up to 90 days could be claimed.

- It includes hospitalisation expenses such as room charges, nursing costs, boarding charges, anaesthetist's fee, specialist's fees, surgeon's fees, cost of drugs, pacemakers, and medicines.

- AYUSH hospitalisation expenses like Homoeopathy, Ayurveda, Unani and Siddha are payable below this plan.

- Expenses for the normal and cesarean delivery could also be claimed.

- It includes newborn babies and vaccination expenses.

- It also includes emergency road ambulance transportation charges.

- Organ donor charges are also covered.

- During emergencies, air ambulance charges are also covered.

- Domiciliary hospitalisation charges are also included under this policy.

- Health checkup facilities expenses are included below this plan.

- Also, the accidental death and permanent total disability claims could be claimed by the insured person.

- Dental/ophthalmic OPD treatment charges are covered once every 3 years.

- Bariatric surgery charges could be claimed after the completion of the waiting period of 3 years.

- The second medical opinion availed from the Star Health Insurance network of doctors can be reimbursed.

- The advantage of hospital cash is that it is offered for up to 7 days in case of hospitalisation.

Exclusions of the Star Comprehensive Health Insurance Plan

Star Comprehensive Health Insurance Plan has some exclusions.

- Cost of Change of Gender treatments.

- Obesity Treatment Costs.

- Pre-existing conditions till the completion of the waiting period of 3 years

- Expenses related to hazardous or adventure sports-related injuries

- Expenses related to unproven treatments

- Infertility and sterility treatment Charges.

- Charges for Venereal diseases and STDs (Other than HIV)

- Costs of Nuclear weapons and war-related perils.

- Expenses for the treatment of endocrine disorders.

- Some factors help you choose comprehensive health insurance in India.

How to choose comprehensive health insurance in India?

Many factors help choose health insurance in India. While you select comprehensive medical insurance in India, you could consider the following factors:

- Claim Settlement Ratio: Always choose health insurance with a high claim settlement ratio.A high claim settlement ratio denotes the insurer's reliability and efficiency in settling claims.

- Network Hospitals: Prefer network hospitals in your place for better access to quality healthcare. For that, see the list of network hospitals under the list of health insurance providers.

- Coverage Offered: To choose the right coverage, start by looking at your healthcare needs and pick a plan that covers most of them in one policy.

- Sum Insured: Analyse the sum insured by various health insurance plans. If you go for a sum insured lower than what is needed for you, it may not be correct for you. Ensure that the sum insured is adequate to cover your maximum medical expenses.

- Co-Payment: Some of the plans only have a mandatory co-pay clause, which requires the policyholders to pay a percentage of every claim.

- Comparison of Many Health Plans: Do proper research and compare various health insurance policies to choose the one that matches your needs. You could compare the plans based on things like benefits, sum insured and add-ons.

- Premiums: Check the premium amount and deductibles related to the health insurance plans. You could pay your health insurance premiums according to your entry age.

- Lifetime Renewability: Choose health insurance plans with lifetime renewability so you stay covered as you get older and may need more medical care.

- Insurer Reviews and Customer Ratings: When you buy health insurance, just review the insurer reviews and customer ratings. Check for the reputation and credibility of the insurance provider prior to buying a health insurance plan.

- Claim Settlement Time: Check each health insurer's claim settlement time before investing in the health plan for yourself. Opting for an insurer with a high claim settlement ratio helps with reliable claim processing.

- Cumulative Bonuses: You get a cumulative bonus for having claim-free policy years. You can have the advantage of this bonus by raising your sum insured while you renew the health policy.

- Higher Sub-Limits: Choose a health insurance plan that has higher or no sub-limits for most categories of expenses. Additionally, they may have to choose from sub-limits, co-payments or voluntary deductibles to minimise the cost of high premiums.

- Policy Exclusions and Limitations: It is necessary to consider the exclusions and limitations when you choose a health insurance policy.

- Pre-Existing Ailments: Ensure that all the pre-existing ailments are disclosed, and see the coverage for the same. Know about the waiting period for pre-existing diseases in the policy chosen.

- Choose Family Floater Plans: If you wish to buy insurance for the whole family, then select a family floater plan rather than buying individual health policies. Select the appropriate plan based on the people to be insured.

Tax Benefits from Buying a Star Comprehensive Insurance Policy

With respect to the premium payment by any mode other than cash, the insured person is eligible for relief under Section 80D of the Income Tax Act of 1961.

Waiting Period Applicable Under Star Comprehensive Health Plan

- The initial waiting period is 30 days.

- The waiting period applicable for the specified disease/ procedure is 24 months

- Waiting period for pre-existing disease is 36 months

- 24 months waiting period applies for delivery expenses and the newborn

- You must complete a waiting period of 36 months for bariatric surgery

Conclusion

The Star Comprehensive Insurance policy is available for both individuals and families, and provides coverage for medical expenditures based on the terms and conditions.

HELP CENTRE

Confused? We’ve got the answers

We’re Star Health. We offer the coverage that’s designed to help keep you healthy. It's the care that comes to you, and stays with you.

FAQ

People Also Search For

Health Insurance Coverage for pre-existing medical conditions is subject to underwriting review and may involve additional requirements, loadings, or exclusions. Please disclose your medical history in the proposal form for a personalised assessment.

The information provided on this page is for general informational purposes only. Availability and terms of health insurance plans may vary based on geographic location and other factors. Consult a licensed insurance agent or professional for specific advice. T&C Apply. For further detailed information or inquiries, feel free to reach out via email at marketing.d2c@starhealth.in