Wellness Program

Take part in our wellness programs and earn rewards for staying healthy. Redeem those rewards to avail renewal discounts.

Top-up Policy

This super top up health insurance policy can be opted along with the existing policy to avail additional Sum Insured at an affordable premium.

Flexible Policy

This policy can be opted on an Individual or Floater basis with 7 family size options (i.e. 2A, 2A+1C, 2A+2C, 2A+3C, 1A+1C, 1A+2C, 1A+3C).

Long-Term Discount

If the policy is opted for a term of 2 years, then 5% discount on premium can be availed.

Medical Examination

Pre-insurance medical screening is not mandatory to avail this policy.

Instalment Options

This policy premium can be paid on a quarterly or half-yearly basis.

Individual Entry Age

Any person aged between 18 and 65 years can avail this policy.

Floater Entry Age

Any person aged between 18 and 65 years can avail this policy. Dependent children are covered from the 91st day onwards up to 25 years.

Detailed List

Policy Term

This policy can be availed for a term of one or two years.

Lifelong Renewal

This policy provides a lifelong renewal option.

In-Patient Hospitalisation

Hospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered.

Pre-Hospitalisation

In addition to in-patient hospitalisation, the medical expenses incurred up to 60 days before the date of admission to the hospital are also covered.

Post-Hospitalisation

Post-hospitalisation medical expenses up to 90 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause.

Room Rent

Room (Single Private A/C room), boarding and nursing expenses incurred during in-patient hospitalisation are covered.

Road Ambulance

Ambulance charges including private ambulance incurred for transporting the insured person to the hospital are covered up to Rs. 3000/- per policy period.

Air Ambulance

Air Ambulance expenses are covered up to 10% of the Sum Insured applicable for Sum Insured of Rs. 7 lakhs and above.

Modern Treatment

Modern treatment expenses incurred either as an in-patient hospitalisation or day care treatment are payable to the extent of the sub-limits mentioned in the policy clause.

Delivery Expenses

Delivery expenses including the Caesarean section are covered up to Rs. 50,000/- per delivery to the maximum of two deliveries. This can be availed after a 12 month waiting period.

Organ Donor Expenses

Organ transplantation expenses are payable subject to the availability of the Sum Insured if the insured person is the recipient.

Recharge Benefit

On exhaustion of the Sum Insured for the remaining policy period, an additional indemnity is provided once during the policy period up to the specified limits.

Wellness Services

Wellness programs designed to motivate and encourage the healthy lifestyle of the insured person through various wellness activities.

E-Medical Opinion

E-Medical Opinion facility from the Company’s expert panel is available on the request initiated by the insured person.

Defined Limit

Defined limit means the amount up to which the company will not be liable during the policy period.

AYUSH Treatment

Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured.

In-Patient Hospitalisation

Hospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered.

Pre-Hospitalisation

In addition to in-patient hospitalisation, the medical expenses incurred up to 30 days before the date of admission to the hospital are also covered.

Post-Hospitalisation

Post-hospitalisation medical expenses up to 60 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause.

Room Rent

Room (including single standard A/C room), boarding and nursing expenses incurred during in-patient hospitalisation are covered up to Rs. 4000/- per day.

Modern Treatment

Modern treatment expenses are payable to the extent of the sub-limits mentioned in the policy clause.

Deductible

Deductible means the amount up to which the company will not be liable for each and every hospitalisation.

AYUSH Treatment

Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured.

In-Patient Hospitalisation

Hospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered.

Pre-Hospitalisation

In addition to in-patient hospitalisation, the medical expenses incurred up to 60 days before the date of admission to the hospital are also covered.

Post-Hospitalisation

Post-hospitalisation medical expenses up to 90 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause.

Room Rent

Room (including single private A/C room), boarding and nursing expenses incurred during in-patient hospitalisation are covered.

Air Ambulance

Air Ambulance expenses are covered up to 10% of the Sum Insured applicable for Sum Insured of Rs. 10 lakhs and above.

Road Ambulance

Ambulance charges including private ambulance incurred for transporting the insured person to the hospital are covered up to Rs. 3000/- per policy period.

Modern Treatment

Modern treatment expenses are payable to the extent of the sub-limits mentioned in the policy clause.

Delivery Expenses

Delivery expenses including the Caesarean section are covered up to Rs. 50,000/- per delivery to the maximum of two deliveries. This can be availed after a 12 month waiting period.

Organ Donor Expenses

Organ transplantation expenses are payable subject to the availability of the Sum Insured if the insured person is the recipient.

Recharge Benefit

On exhaustion of the Sum Insured for the remaining policy period, an additional indemnity is provided once during the policy period up to the specified limits that can be used even for same hospitalisation.

E-Medical Opinion

E-Medical Opinion facility from the Company’s expert panel is available on the request initiated by the insured person.

Wellness Services

Wellness programs designed to motivate and encourage the healthy lifestyle of the insured person through various wellness activities.

Defined Limit

Defined limit means the amount up to which the company will not be liable during the policy period.

AYUSH Treatment

Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured.

In-Patient Hospitalisation

Hospitalisation expenses incurred for a period of more than 24 hours on account of illness, injury or accidents are covered.

Pre-Hospitalisation

In addition to in-patient hospitalisation, the medical expenses incurred up to 30 days before the date of admission to the hospital are also covered.

Post-Hospitalisation

Post-hospitalisation medical expenses up to 60 days from the date of discharge from the hospital are covered as per the limits mentioned in the policy clause.

Room Rent

Room (Single Standard A/C Room), boarding and nursing expenses incurred during in-patient hospitalisation are covered up to Rs. 4000/- per day.

Modern Treatment

Modern treatment expenses are payable to the extent of the sub-limits mentioned in the policy clause.

Deductible

Deductible means the amount up to which the company will not be liable for each and every hospitalisation.

AYUSH Treatment

Medical expenses for Inpatient Hospitalization incurred on treatment under Ayurveda, Unani, Sidha and Homeopathy systems of medicines in a AYUSH Hospital is payable up to the sum insured.

Waiting Period

1. For Pre-Existing Diseases (Silver Plan) - 36 months

2. For Pre-Existing Diseases (Gold Plan) - 12 months

3. For Specific Diseases/Procedures (Silver Plan) - 24 months

4. For Specific Diseases/Procedures (Gold Plan) - 12 months

5. Initial Waiting Period - 30 days (Except for Accidents)

Modern Treatments

Coverage for Modern Treatments on Individual basis please click here.

Coverage for Modern Treatments on Floater basis please click here.

Individual Benefits

Silver Plan | Gold Plan |

|---|---|

Sum Insured on Individual Basis

|

Sum Insured on Individual Basis.

|

In-Patient Hospitalization Expenses: Room, Boarding and Nursing expenses subject to a maximum of Rs.4,000/- per day.

|

In-Patient Hospitalization Expenses : Room (Single Private A/C Room), Boarding and Nursing expenses.

|

Surgeon’s fees, Consultant’s fees, Anesthetist’s and Specialist’s fees.

|

Surgeon’s fees, Consultant’s fees, Anesthetist’s and Specialist’s fees.

|

Anesthesia, Blood, Oxygen, ICU Charges and Operation Theatre charges, Cost of Pacemakers.

|

Anesthesia, Blood, Oxygen, ICU Charges and Operation Theatre charges, Surgical Appliances, Medicines and Drugs, Diagnostic Materials, X-ray and Cost of Pacemakers.

|

Pre and Post Hospitalization – 30 days and 60 days

|

Pre and Post Hospitalization – 60 days and 90days.

|

Pre-Existing Diseases / Illness: Covered after 36 months of continuous Insurance without break with Insurer

|

Pre Existing Diseases: Covered after 12 months of continuous coverage without break with Insurer.

|

Waiting period for Specific diseases – 24 months

|

Waiting period for Specific diseases – 12 months.

|

Deductible applied for each and every claim |

The Proposer can opt at the beginning of 6th year before renewal of this policy or later during any successive renewal , for an Indemnity Health Insurance policy without defined limit offered by the Company with continuity of benefits for the average sum insured of immediately preceding 5 years period subject to the following :- All the Insured Persons are insured with the Company under this policy before the age of 50 years and have been continuously renewed without any break No claim has been made during the immediately preceding 5 years. The proposer should exercise this option for all the insured persons. This policy shall not be further renewed if the option is exercised.

|

Coverage for Modern treatment : Up to the limits mentioned in the policy

|

Delivery Expenses: Expenses for a Delivery including Delivery by Caesarean section (including pre-natal, post-natal expenses and lawful medical termination of pregnancy) up-to Rs.50,000/- per policy period, subject to a maximum of 2 deliveries in the entire life time of the insured person are payable while the policy is in force.

|

Long term and Instalment Facility is available

|

Organ Donor Expenses for organ transplantation where the insured person is the recipient are payable provided the claim for transplantation is payable and subject to the availability of the sum insured. Donor screening expenses and post-donation complications of the donor are not payable.

|

|

Recharge Benefit : If the sum insured under the policy is exhausted/ exceeded during the policy period, additional indemnity up to the limits stated in the policy would be provided once for the remaining policy period.

|

|

Emergency ambulance charges for transporting the insured patient to the hospital up to Rs.3,000/- per policy period.

|

|

Air Ambulance cover: Up to 10% of the sum insured per policy period for Sum Insured of Rs.7 lacs and above.

|

|

Facility of obtaining E-Medical opinion.

|

|

Coverage for Modern Treatment up to limits mentioned in the policy.

|

|

Wellness service

|

|

Long term and Instalment Facility is available.

|

Floater Benefits

Silver Plan | Gold Plan |

|---|---|

Sum Insured on Floater Basis

|

Sum Insured on Floater Basis |

In-Patient Hospitalization Expenses: Room, Boarding and Nursing expenses subject to a maximum of Rs.4,000/- per day. |

In-Patient Hospitalization Expenses : Room (Single Private A/C Room), Boarding and Nursing expenses |

Surgeon’s fees, Consultant’s fees, Anesthetist’s and Specialist’s fees.

|

Surgeon’s fees, Consultant’s fees, Anesthetist’s and Specialist’s fees. |

Anesthesia, Blood, Oxygen, ICU Charges and Operation Theatre charges, Cost of Pacemakers.

|

Anesthesia, Blood, Oxygen, ICU Charges and Operation Theatre charges, Surgical Appliances, Medicines and Drugs, Diagnostic Materials, X-ray and Cost of Pacemakers.

|

Pre and Post Hospitalization – 30 days and 60 days.

|

Pre and Post Hospitalization – 60 days and 90days.

|

Pre-Existing Diseases / Illness: Covered after 36 months of continuous Insurance without break with Insurer.

|

Pre Existing Diseases: Covered after 12 months of continuous coverage without break with Insurer.

|

Waiting period for Specific diseases – 24 months.

|

Waiting period for Specific diseases – 12 months |

Deductible applied for each and every claim. |

The Proposer can opt at the beginning of 6th year before renewal of this policy or later during any successive renewal , for an Indemnity Health Insurance policy without defined limit offered by the Company with continuity of benefits for the average sum insured of immediately preceding 5 years period subject to the following :- All the Insured Persons are insured with the Company under this policy before the age of 50 years and have been continuously renewed without any break No claim has been made during the immediately preceding 5 years. The proposer should exercise this option for all the insured persons. This policy shall not be further renewed if the option is exercised.

|

Coverage for Modern treatment : Up to the limits mentioned in the policy

|

Delivery Expenses: Expenses for a Delivery including Delivery by Caesarean section (including pre-natal, post-natal expenses and lawful medical termination of pregnancy) up-to Rs.50,000/- per policy period, subject to a maximum of 2 deliveries in the entire life time of the insured person are payable while the policy is in force.

|

Long term and Instalment facility is available.

|

Organ Donor Expenses for organ transplantation where the insured person is the recipient are payable provided the claim for transplantation is payable and subject to the availability of the sum insured. Donor screening expenses and post-donation complications of the donor are not payable.

|

Recharge Benefit: If the sum insured under the policy is exhausted/ exceeded during the policy period, additional indemnity up to the limits stated in the policy would be provided once for the remaining policy period.

| |

Emergency ambulance charges for transporting the insured patient to the hospital up to Rs.3,000/- per hospitalization.

| |

Air Ambulance cover: Up to 10% of the sum insured per policy period for Sum Insured of Rs.10 lacs and above.

| |

Facility of obtaining E-Medical opinion.

| |

Coverage for Modern Treatment up to limits mentioned in the policy.

| |

Wellness service

| |

Long term and Instalment facility is available.

|

Free Look Period

The Free Look Period shall be applicable on new individual health insurance policies and not on renewals or at the time of porting/migrating the policy.

The insured person shall be allowed free look period of thirty days from date of receipt of the policy document whether electronically or otherwise to review the terms and conditions of the policy, and to return the same if not acceptable.

i. If the insured has not incurred any claim during the Free Look Period, the insured shall be entitled to a refund of the premium paid less any expenses incurred by the Company on medical examination of the insured person and the stamp duty charges or

ii. where the risk has already commenced and the option of return of the policy is exercised by the insured person, a deduction towards the proportionate risk premium for period of cover or

iii. where only a part of the insurance coverage has commenced, such proportionate premium commensurate with the insurance coverage during such period

As a Health Insurance specialist, we extend our services from offering tailor-made products to fast in-house claim settlements. With our growing network of hospitals, we ensure easy access to fulfill your medical needs.

Take part in our wellness programs and earn rewards for staying healthy. Redeem those rewards to avail renewal discounts.

Get access to 1,635 diagnostic centres across India with home pickup of lab samples and health checkups at your doorstep.

Order medicines online at a discounted price. Home delivery and store pick-ups are available across 2780 cities.

Call us at 1800-425-2255 for claim intimation, telehealth services, and to clear your queries.

We’re the first Standalone Health Insurance company to settle the claims without any TPA but with a qualified in-house team.

90% of our claims are settled under cashless within 2 hours and 92% of claims are settled under reimbursement within 7days.

We got you covered under our valuable service providers, an agreed network and network hospitals for quality treatment.

We’ve been awarded for innovative product, best claim settlement and service provider from reputed survey organisations.

Hospitals in agreement with Star Health provide seamless cashless facilities. The approval process is quick and comfortable.

Hospitals that have agreed with Star Health to provide cost-effective package rates for surgical and medical procedures.

These hospitals are identified by Star Health and have been specially recognised for their efforts, services and quality.

For getting treatments in non-network hospitals(not in agreement with Star Health), you can avail reimbursement claims.

Hospitals, where claims are not admissible. But life-threatening situations/accidents expenses are payable up to stabilisation.

Get your future secured with us.

“Insurance for Health is Wealth” has become a prominent term in our fast-paced world today. No matter how conscious we are of our mind and body, a health emergency may come knocking at any point in life. You must ensure that you are well-prepared for such circumstances.

A health insurance policy helps you get timely treatment while facing an illness/injury. Even with a standard health insurance policy, rising medical costs can quickly exceed a sum insured of 5–10 lakhs. In such cases, a top-up health insurance plan works as a supplement to your regular health insurance cover. This plan adds additional coverage to your existing health insurance policy. In simple words, a top-up health insurance plan activates once your base policy reaches its coverage limit, offering extended protection.

Star Health Super Surplus Policy is a premium health insurance plan that provides much more coverage than standard health insurance plans. The policy is available on a floater and individual basis, and individuals between the ages of 18 and 65 are eligible to purchase the policy.

When purchased on a floater basis, the policy can cover self, spouse, and dependent children. The policy offers a higher sum insured at an affordable premium, making it a preferred choice for many.

For those seeking to enhance their medical insurance affordably, the Star Health Super Surplus top-up plan is an excellent choice.

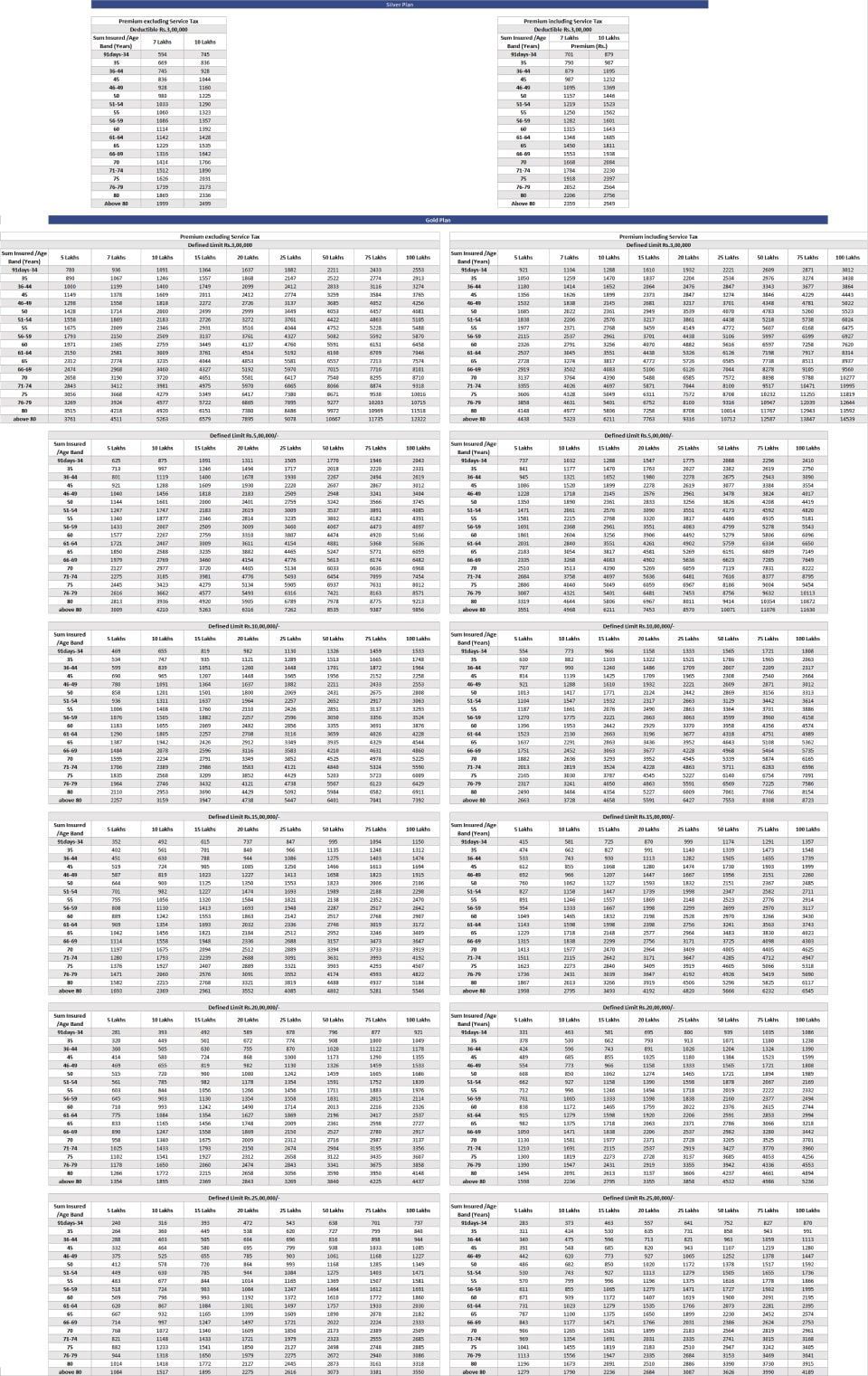

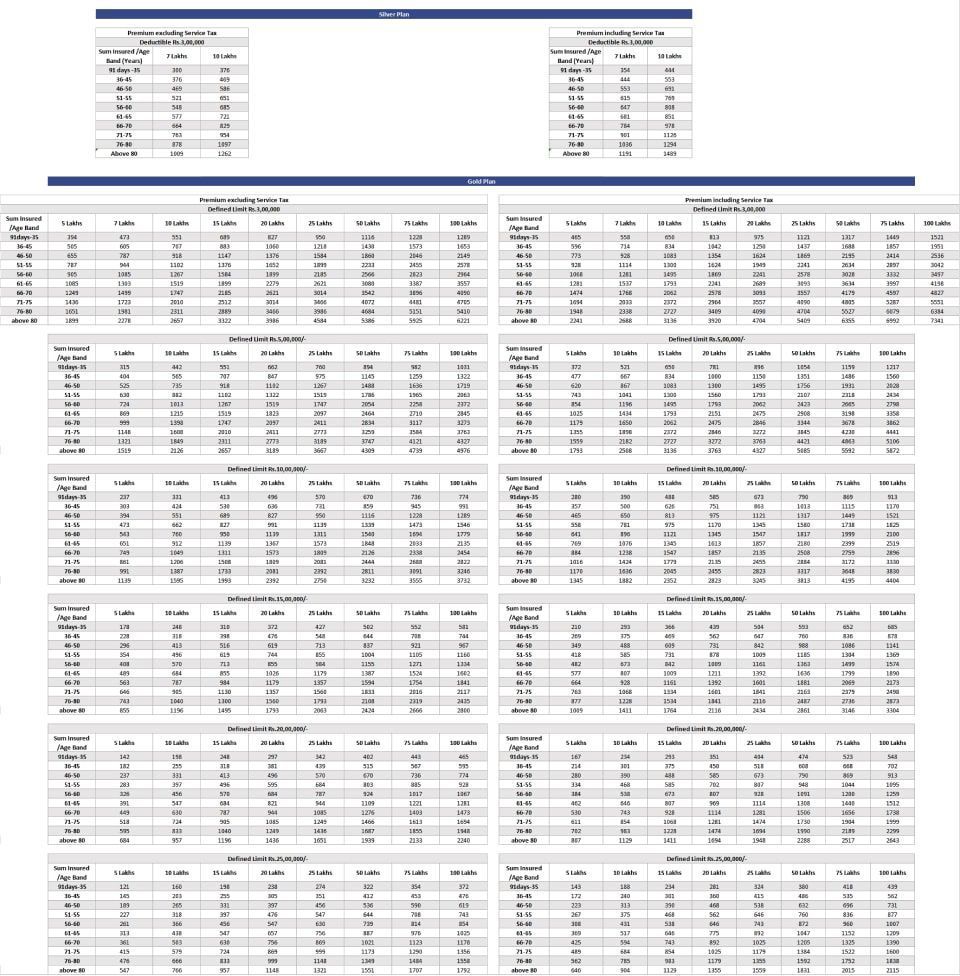

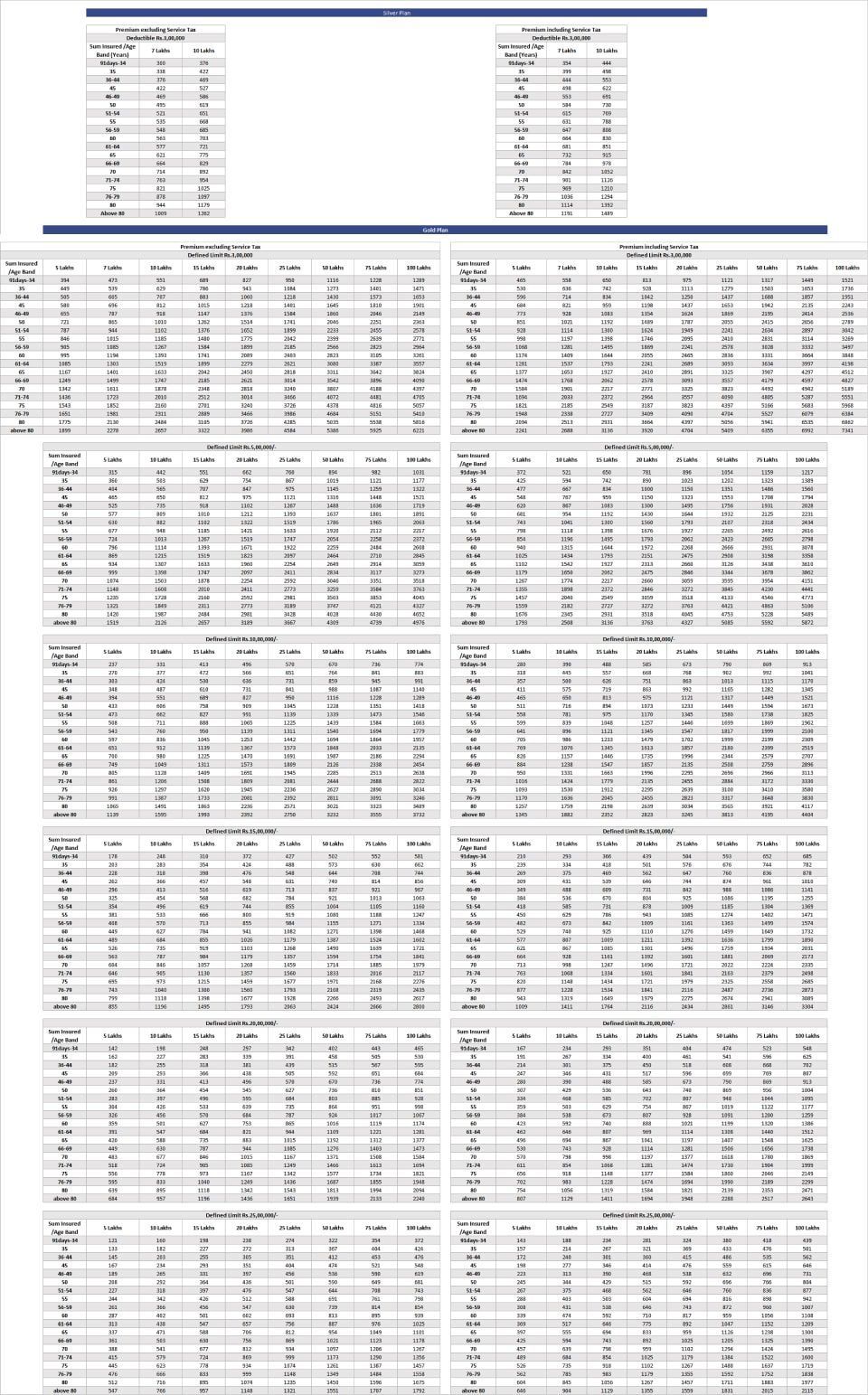

The Star Health Super Surplus policy is available in two plans: Silver Plan and Gold Plan. The policy covers organ donor expenses, daycare treatments, ambulance charges, inpatient hospitalisation expenses, pre-hospitalisation, and post-hospitalisation expenses.

A super top-up health insurance plan kicks in once the total medical expenses within a policy year exceed the deductible limit.

For instance, if you have a base health plan with a sum insured of Rs. 5 lakhs and an additional super top-up plan of Rs. 3 lakhs. If you are hospitalised, your base health plan will bear the costs of medical bills up to Rs. 5 lakhs, and the top-up plan will kick in after the maximum sum assured by your base plan has been crossed.

A health insurance top-up is an additional coverage plan that supplements your existing health insurance policy. It comes into effect once your base policy’s sum insured is exhausted, offering financial protection against high medical expenses without the need to upgrade your primary plan.

A top-up health insurance plan offers extra medical coverage for individuals already covered by a personal or employer-provided health policy.

This type of insurance enhances your existing individual or group mediclaim policy by offering additional medical coverage. It enhances the degree of financial security you have against different health-related concerns and expands the sum insured amount.

If your health insurance policy does not provide enough coverage to meet high hospitalisation bills, you may have to purchase two insurance policies or increase the sum assured amount.

Whether you're looking to protect your savings or prepare for rising healthcare costs, a health insurance top-up is a smart and affordable way to boost your coverage. Select a top-up health insurance plan that aligns with your needs and strengthens your financial protection against medical expenses.

Suppose you have a health plan with a maximum sum assured of Rs. 10 lakhs, and you take a top-up plan for Rs. 4 lakhs. If you're hospitalised, your base plan will cover expenses up to Rs. 10 lakhs, and the top-up plan will cover costs beyond that limit.

A top-up health insurance plan is an add-on cover that increases the health insurance coverage for the policyholder.

When medical bills exceed your insurance coverage, out-of-pocket expenses can threaten financial stability. In such cases, top-up plans offer valuable support.

Star Health’s Super Surplus Insurance policy offers coverage up to one crore at an affordable premium, making it a strong supplement to your existing health plan. It provides broader protection compared to standard health insurance plans. The policy is available for the age group from three months to 65 years on both an individual and a floater basis.

The policy is available in options as Gold and Silver plans. The waiting period under this policy is 12 months and 36 months, respectively. The policy terms are one year/2 years. On the policy purchase, a lifelong renewability option is available.

Yes, a person can top up his/her health insurance policy to offer extra coverage. A top-up health insurance policy is an add-on to your existing health insurance plan. It provides extra coverage once your medical expenses exceed a certain deductible. We have seen what a top-up in health insurance is; let’s see how to top up health insurance.

You can avail a top-up health insurance in two ways, either as a top-up health plan or as a super top-up health plan. Both of these ways function as a booster to your primary health insurance policy. These plans could be used to pay the extra medical expenses if your regular health policy gets exhausted.

Know how to take a top-up health insurance. As mentioned above, the top-up health insurance is an extra health coverage that you could add to a good health insurance policy that you have.

In our country, in some cases, your basic health plan might not be sufficient, as there is an increase in lifestyle ailments and medical inflation due to modernisation. In India, top-up health insurance can help bridge the gap caused by rising medical costs and lifestyle-related illnesses.

Hence, choosing a top insurance alone is not enough; you could also select the best top-up health insurance. Here, we have already discussed top-up health insurance benefits.

When you check what the top health insurance company is, also check the details of the top-up health insurance provided by those companies. Explore the best insurance plan and the best top-up health insurance that suits your medical and financial needs.

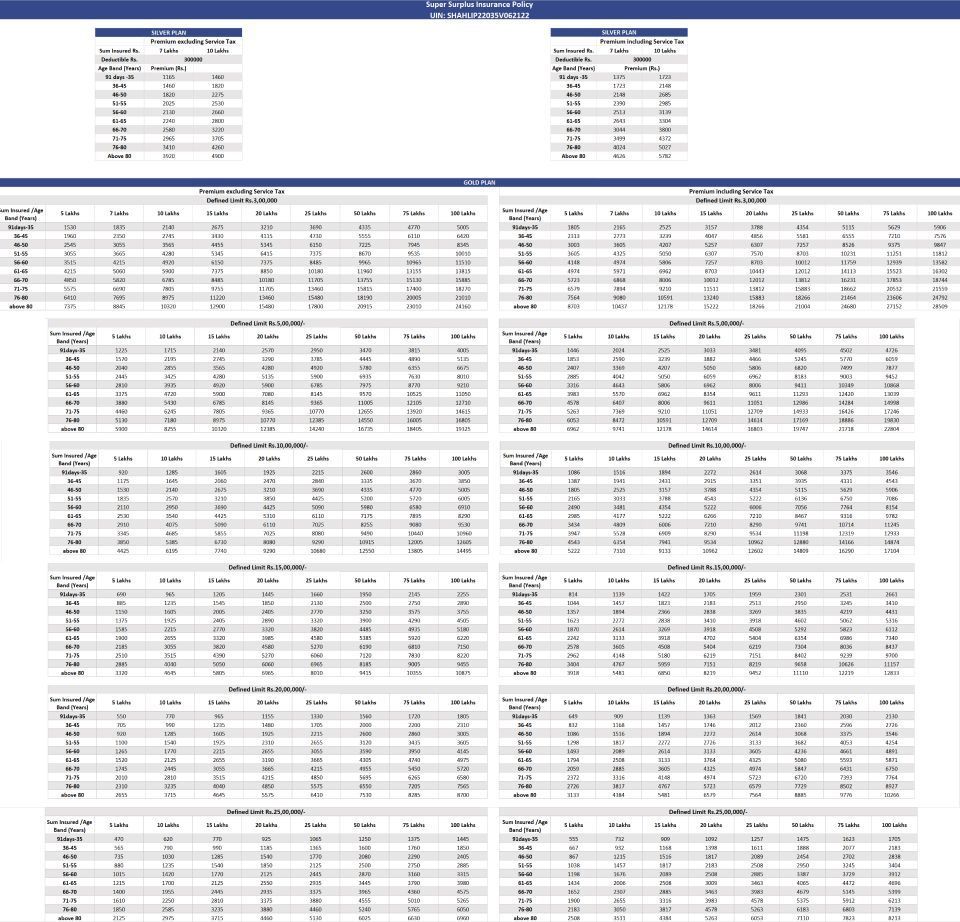

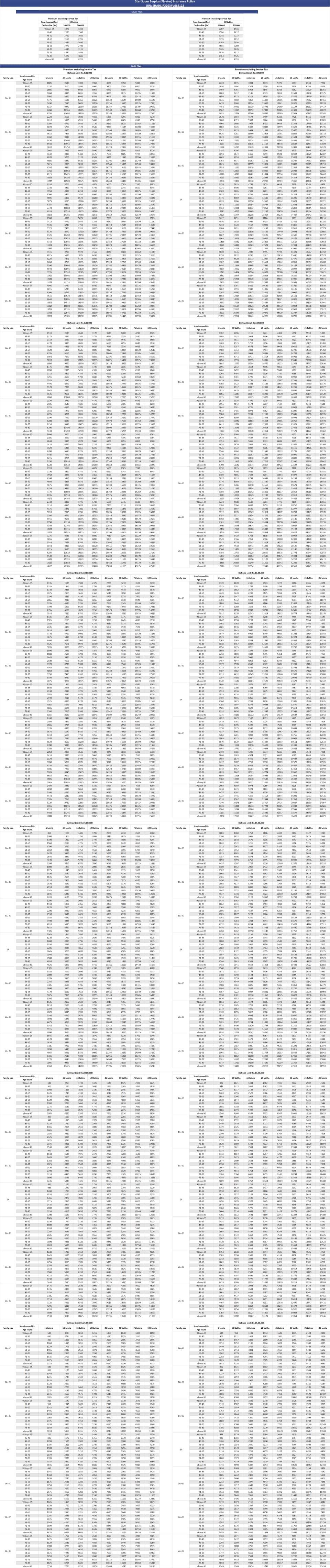

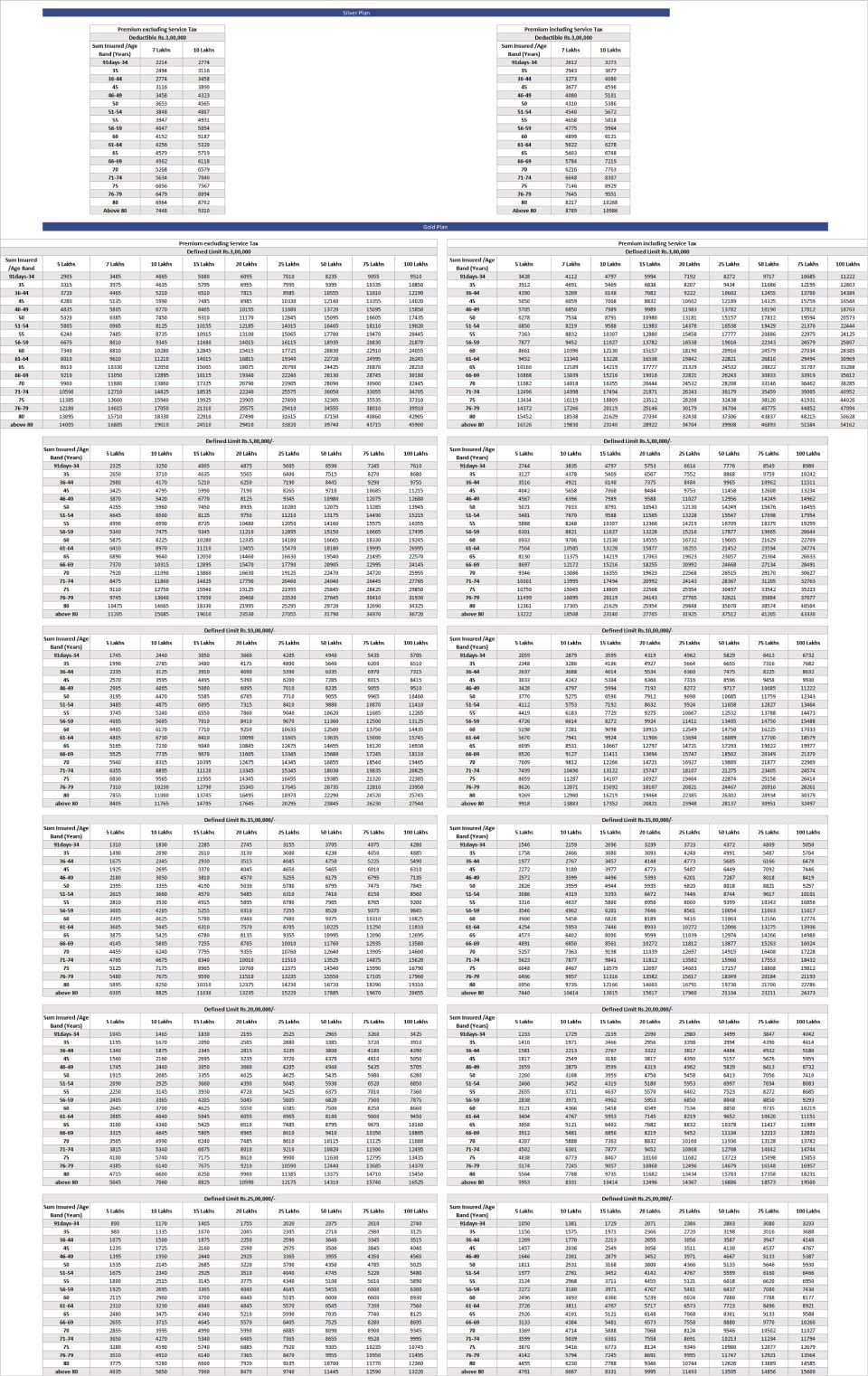

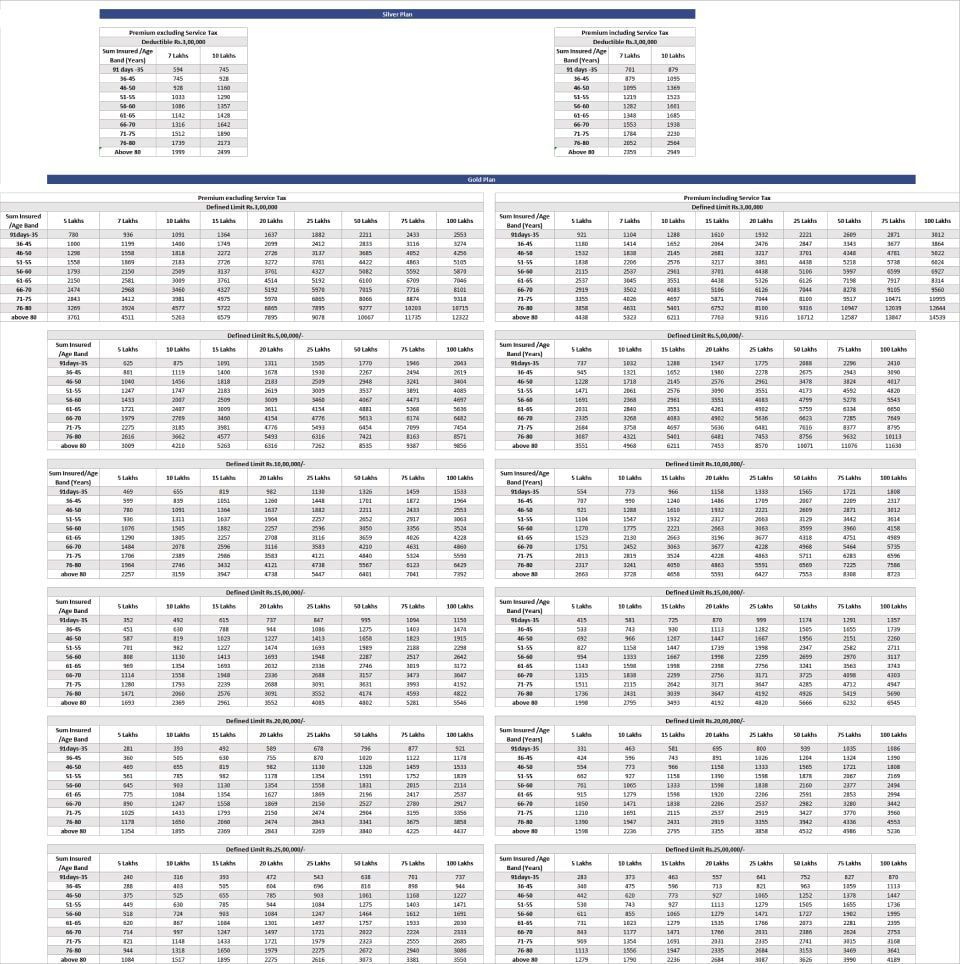

| S.No | Subject | Criteria | ||

|---|---|---|---|---|

| 1. | Eligibility | 18-65 years | ||

| 2. | Dependent children | 91 days to 25 years | ||

| 3. | Policy term | 1 / 2 years | ||

| 4. | Plan options | Silver / Gold plan | ||

| 5. | The Company will pay in excess of the deductible limit on every claim under Silver plan | Silver | Sum insured | Deductible limit |

| Individual | 7 lakhs / 10 lakhs | 3 lakhs | ||

| Floater | 10 in lakhs | 3 & 5 lakhs | ||

| The Company will pay the aggregate of all claims amount in excess of defined limit in the policy year under Gold plan | Gold | Sum insured | Defined limit | |

| Individual | 5 / 10 / 15 / 20 / 25 /50 / 75/ 100 lakhs | 3 / 5 /10 / 15 / 20 /25 lakhs | ||

| Floater | ||||

| 6. | Product type | Individual / Floater | ||

| 7. | Installment facility | Quarterly / Half-yearly | ||

| 8. | Discounts | 5 percent discount only if the entire two-year premium is paid in advance | ||

| 9. | Renewals | Life-long renewal option | ||

| 10. | Pre-insurance medical screening | Not required | ||

The policy offers extensive coverage for both individual and floater under two plan options, namely Gold and Silver. You can use the super top-up health insurance premium chart to compare Gold and Silver plan options by coverage and cost. These top-up health insurance plans offer flexibility for both individual and floater coverage, ensuring tailored protection.

This benefit is elaborated as follows:

A top-up mediclaim policy is ideal for individuals who want to extend their coverage without replacing their existing plan. To understand the working of top-up policies, you should know two terms: one is Deductible & Defined Limit (Aggregate Deductible)

Case Study : Top-up health insurance is especially useful when your primary policy has a lower sum insured. For example, if the insured has a top-up policy with a sum insured of 10 lakhs and a deductible of 1 lakh, the plan provides additional coverage beyond the deductible.

| Period of Claim Claims during the same year | Claims during the same year | Sum Insured (Deductible) | Insured to pay for each Claim | Admissible claim Amount Payable | Amount payable | Balance Sum insured available for future claim |

| 21- 22 | 1st | 10 lakhs (1L) | 1 Lakh | 5 Lakhs | 4 Lakhs | 6 lakhs |

| 21- 22 | 2nd | 6 Lakhs (1L) | 1 Lakh | 3 lakhs | 2 lakhs | 4 lakhs |

| 21- 22 | 3rd | 4 Lakhs (1 L) | 1 Lakh | 4 lakhs | 3 lakhs | 1 lakh |

| 21- 22 | 4th | 1Lakhs (1L) | 1 Lakh | 2 lakhs | 1 lakh | nil |

| Period of Claim | Claims during the same year | Sum Insured (Defined ) | Insured to pay for per policy period | Admissible claim Amount Payable | Amount payable | Balance Sum insured available for future claim |

| 21- 22 | 1st | 10 lakhs (1 lakh) | 1 Lakh | 5 Lakhs | 4 Lakhs | 6 lakhs |

| 21- 22 | 2nd | 6 lakhs | Nil | 3 Lakhs | 3 lakhs | 3 lakhs |

| 21- 22 | 3rd | 3 Lakhs | Nil | 3 Lakhs | 3 lakhs | nil |

In this case, the health insurance top-up plan activates once the deductible of ₹1 lakh is met.

Investing in a top-up health insurance plan not only provides financial freedom but also a sense of security, ensuring peace of mind.

Health insurance specialists say that a top-up plan is a must-have. For instance, the current pandemic has caused a major financial hardship during hospitalisation. However, buying a top-up plan is much better than extending your existing basic health insurance cover at a nominal cost. Top-up health insurance plans are designed to provide additional cover if your existing policy gets exhausted.

The Super Surplus insurance policy comes with certain inclusions (covered) and exclusions (not covered). They are as follows:

Inclusions

Exclusions

The following is a partial listing of policy exclusions. A detailed list of all exclusions is included in the policy document.

A top-up health insurance plan prepares you for increasing and dynamic costs of hospitalisation. It is similar to that of any regular health insurance plan. This plan is payable towards treatment expenses for illness or accidents in a hospital or day-care centre. The maximum amount policyholders must pay is deductible before their insurer covers the losses. A higher deductible lowers the premium. The waiting period for pre-existing and specified illnesses is 12 months from the policy's inception under the defined limit.

A top-up health insurance plan offers extra coverage to the existing health insurance policy and helps to cover medical expenses that exceed the sum insured of the regular health insurance policy. The top-up policy works on the principle of the deductible.

The top-up plan ensures access to quality medical care without extra costs and lets you increase the sum insured at minimal expense.

Top-up health insurance plans cover almost all hospitalisation expenses and provide the same benefits as a basic health plan. The key difference is the deductible, which makes these plans more affordable. Most top-up plans do not require pre-medical screening up to the age of 50 years, which is mandatory after 45 years under most basic health insurance plans.

If your basic health plan reaches the sum insured limit, you can file a claim under both your base plan and top-up plan together. Moreover, you can easily file a claim under both plans simultaneously with insurance providers, who will be liable to pay off part of their claims.

Inpatient hospitalisation expenses

In-patient hospitalisation expenses, including nursing and boarding charges, room rent, doctors’ fees, OT charges, cost of oxygen, prosthetic devices or implantation of any other equipment during surgery, blood, diagnostic procedures and other similar expenses.

Primary things to look for when buying top-up insurance

To select an affordable top-up health insurance plan, opt for higher deductibles. Avoid buying an expensive plan to cover exclusions like daily cash allowance and dental cover, as they may be covered by your regular health insurance policy.

A mediclaim top-up plan can help bridge the gap between your employer-provided coverage and actual medical expenses. There are several top medical insurance companies in India to choose from. When you choose a medical insurance company in India, you can consider factors like:

When choosing medical insurance, you can consider some factors, such as your needs, coverage, and the insurance provider.

By considering all these factors, you could shortlist the top medical insurance companies in India. Then, choose the best one out of the top medical insurance companies in India.

Star Health offers hassle-free claim settlement for all its customers. There are two ways through which you can file a claim at your convenience.

Top-up health insurance is a cost-effective way to increase medical coverage. It is advisable to choose a policy with an aggregate deductible and the lowest possible waiting period for pre-existing disease coverage. This helps manage rising medical costs and bridge gaps in corporate, individual, or family health insurance plans.

The insurance coverage under this policy for each insured person will expire upon the earliest of the following events:

Top-up medical insurance is a smart way to extend your coverage without purchasing a new base policy.

The Policyholder may cancel his Super Surplus policy at any time during the term by providing a 7-day written notice. In such a case, the Company may :

The Company may cancel the policy at any time due to misrepresentation, non-disclosure of material facts, or fraud by the insured person, by providing 15 days’ written notice. Also, there will be no refund of premium on cancellation on the basis of misrepresentation, fraud or non-disclosure of material facts.

Point to Note: If it is a long-term policy, the refund will be given after adjusting the long-term discount obtained by the insured person/ policyholder.

The insured person has the choice to migrate to the same health insurance product available with the Company during the renewal time, with all the accrued continuity.

Advantages such as cumulative bonus and waiting period waiver, as per IRDAI guidelines, are maintained if the policy has been renewed without a break.

Top-up medical insurance, like this plan, is ideal for individuals and families seeking additional protection beyond their base policy. To ensure comprehensive protection, choose the best top-up health insurance that aligns with your healthcare needs and budget.

The waiting period for pre-existing diseases under the Super Surplus silver plan is 36 months, and for specific treatments, it is 24 months. The waiting period for pre-existing diseases and specific treatments under the Super Surplus gold plan is 12 months.

Yes, all health insurance plans are eligible for a top-up with the Super Surplus policy.

People between the ages of 18 and 65 years can take this policy. Dependent children can be covered from 91 days -25 years.

Yes, the policy covers pre-existing diseases after a waiting period of 36 months (silver plan) and 12 months (gold plan).

No, pre-insurance medical screening is not required for the Super Surplus Insurance policy.

The Super Surplus plan offers coverage on both an individual basis and a floater basis, allowing you to choose the option that best suits your family’s needs.

While you make health insurance top-up plan comparisons, the things to be considered include the deductible amount you choose, the coverage limit (sum insured) given, any extra benefits such as the pre- and post-hospitalisation coverage, the policy's premium amount, and the network hospitals available for cashless treatment. Also, one must check for co-payment clauses, waiting periods, and see the differences between top-up and super top-up plans.

There are many advantages of a mediclaim top up plan. The benefits of a mediclaim top up plan include :

Health insurance top-up plans are needed to offer an extra layer of financial safety when your basic health insurance coverage is insufficient. They help meet the complication of high out-of-pocket expenses resulting from increasing medical costs, serious illnesses, or multiple hospitalisations.

There are many benefits of the best super top up health insurance. The benefits of the best super top up health insurance include coverage for the in-patient hospitalisation expenses, pre- and post-hospitalisation expenses, daycare treatments, ambulance expenses, ICU charges, and organ donor expenses.

It’s a secondary plan that kicks in once your primary coverage is exhausted.

You can apply for additional medical coverage by contacting your insurer or checking the add-on options available in your existing policy. Most insurers let you increase coverage during renewal or by choosing top-up or super top-up plans. You may need to fill out a short form and share updated health details before the new cover is approved.

There is no single best top-up plan because the right one depends on your existing base policy, budget, and the deductible you prefer. A good top-up plan should offer affordable premiums, flexible deductible options, and reliable claim support when your main policy limit gets exhausted.

Yes, a super top-up plan is usually worth it because it gives you high coverage at a low cost. It works well when your main health insurance is not enough or when medical bills cross a certain limit. It also covers multiple claims in a year once the deductible is crossed, which makes it more useful than a regular top-up plan.

Yes, you can buy two super top-up plans. People usually do this when they want higher overall coverage at a lower cost. Just make sure the deductibles and coverage limits are clear so that claims can be processed smoothly without confusion.

ISO 22301

ISO/IEC 27001

ISO 9001:2015

Insurance

Resources

Services

Regulatory

© Star Health Insurance. All rights reserved.

Registered Office: No 1, New Tank Street, Valluvarkottam High Road, Nungambakkam, Chennai 600034

IRDAI Registration No: 129 | CIN : L66010TN2005PLC056649 | Ph: 044-28288800 | Fax: 044-28260062 | Email: info@starhealth.in | Website: www.starhealth.in

Toll Free Number -1800-425-2255 / 1800-102-4477 | Corporate Customers - 044 43664666